Key Takeaways

- With Giniloh Relocation Payback & Tax Adjustment Modeler, you can calculate your specific payback period by dividing the total upfront costs of moving by the monthly increase in your net take-home pay to determine how long it will take to break even.

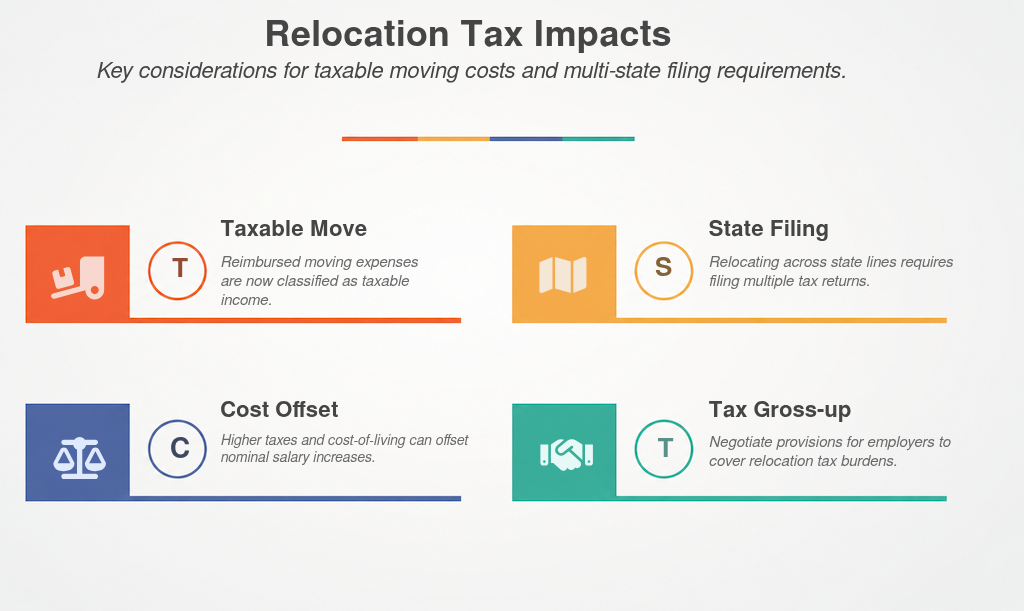

- Negotiate for a tax gross-up provision in your relocation package to ensure your employer covers the federal and state tax liabilities triggered by moving expense reimbursements.

- Account for the loss of federal tax deductions for moving expenses, as current laws treat most employer-provided relocation assistance as taxable income rather than a tax-free benefit.

- Evaluate the impact of state-specific tax structures, such as local piggyback taxes or high marginal rates, which can significantly reduce the purchasing power of a nominal salary increase.

- Prepare for the administrative complexity of filing partial-year tax returns in two different jurisdictions to avoid potential double taxation and ensure accurate income allocation.

Introduction: The High-Stakes Gamble of Career Relocation

The promise of a more prestigious title and a larger paycheck in a dynamic environment is hard to ignore. For a software engineer I advised several years ago, a move from Maryland to California offered a salary jump from $95,000 to $120,000. On paper, this looks like a clear 26.3% win, suggesting a substantial increase in purchasing power.

However, as I dug deeper into the fiscal data, I realized this move involves variables that can quickly erase those gains. Career relocation is rarely just about gross income. It is a multi-layered transaction involving tax law, cost-of-living adjustments, and immediate cash needs. These factors often go overlooked during the initial excitement of a new opportunity.

In my analysis of these transitions, I have found that the “nominal raise” is often a financial illusion. When moving between states with vastly different tax codes and housing markets, the “real wage” tells a different story. Understanding these hidden costs is essential for any professional considering a cross-country move in the current economic climate.

The allure of the West Coast tech scene remains strong, but the economic friction of getting there has never been higher. As the labor market shifts and remote work options fluctuate, the decision to relocate has become a complex exercise in personal finance. For many, the “dream job” can inadvertently lead to a “nightmare budget” if the transition is not managed with surgical precision.

This article helps you uncover the real payback period for this relocation offer example using the Giniloh Relocation Payback & Tax Adjustment Modeler,

The Regulatory Framework of Relocation

Corporate relocation packages often cover moving services, temporary housing, or lease termination fees. While these perks help, federal tax changes have fundamentally altered their value. Under the Tax Cuts and Jobs Act (TCJA) of 2017, the federal treatment of moving expenses underwent a radical shift.

What used to be a tax-free benefit is now a taxable liability for most employees. Previously, qualified moving expenses were deductible from gross income, and employer reimbursements were generally tax-free. This allowed workers to move without incurring a massive tax bill.

However, under current federal law, the IRS treats these reimbursements as taxable income for the recipient. This applies regardless of whether the money went directly to a moving company or into the employee’s pocket as a lump sum. This legislative change means that every dollar a company spends to move your furniture is a dollar you are taxed on.

Table 1: Federal Tax Treatment of Moving Expenses

For a professional moving across the country, these costs can easily exceed $15,000. This creates a significant financial burden at a time when liquidity is already stretched thin. This shift creates a “tax drag” on the moving process that many fail to anticipate. The Giniloh Relocation Payback & Tax Adjustment Modeler considers these scenarios in the calculations.

The Financial Implications of Professional Relocation

Securing a professional offer in a new jurisdiction marks a significant career milestone. Yet, the financial reality of moving often extends far beyond the base salary listed on the contract. Financial advisors report that career-related moves involve complex fiscal challenges that many candidates overlook.

While a higher salary appears advantageous, the actual economic impact depends on shifting factors. These include state tax mandates, federal legislative changes, and regional cost-of-living adjustments. These variables can quickly erode a nominal pay increase.

The transition between states requires a technical approach to tax compliance. Professionals must manage the requirements of two distinct tax authorities, filing partial-year returns in both states. This process is rarely a simple division of income by months spent in each location.

Instead, compliance involves the precise allocation of earnings, deductions, and credits based on specific residency dates. When moving between states with disparate tax structures, a “tax drag” often occurs. This phenomenon can significantly diminish the anticipated financial gains of a promotion.

Taxation of Relocation Benefits and the TCJA

The landscape of corporate relocation shifted with the implementation of the TCJA in 2018. Before this legislation, many moving expenses were deductible for the employee. They could also be reimbursed by the employer on a tax-free basis.

This previous arrangement included the cost of transporting household goods and travel expenses. However, under current federal law, these reimbursements are treated as taxable wages. This change means a relocation package valued at $20,000 is no longer a net benefit of $20,000.

Instead, the IRS views that amount as gross income subject to federal, state, and FICA taxes. For a professional in a high tax bracket, this creates a liability of several thousand dollars. This debt must be settled during the following tax season.

Analysts suggest that without a “gross-up” provision, the employee effectively pays for their own relocation through increased withholding. In a gross-up scenario, the employer provides additional funds specifically to cover these taxes.

This ensures the employee receives the full intended value of the assistance. The IRS maintains strict reporting requirements for these benefits, and employers must include them on the W-2 form. This increase in reported income can have secondary effects on a taxpayer’s filing, such as triggering the phase-out of certain tax credits.

Decoding Career Relocation Assistance: What Job Postings Actually Offer

For many relocating professionals, the promise of a corporate-funded move suggests a seamless transition. However, industry data shows that the “sticker price” of a package rarely matches the actual net benefit.

In the current labor market, the gap between a gross offer and take-home reality can be vast. Understanding the contractual nuances of these agreements is no longer optional. It is a requirement for maintaining financial stability during a cross-country move.

Economic

analysts suggest that the “Great Relocation” trend has shifted how companies view mobility. While remote work initially slowed corporate moves, return-to-office mandates have revitalized the industry. This resurgence has brought a renewed focus on the complex financial instruments used to move talent.

Table 2: Common Relocation Assistance Models

The Architecture of Modern Relocation Assistance

In the contemporary corporate landscape, career relocation packages are far from uniform. While recruiters use the term as a generic benefit, the structure varies based on seniority and industry norms. Most packages fall into four distinct categories: lump-sum, direct billing, managed moves, and reimbursement.

The lump-sum payment is the most frequent choice for entry-to-mid-level roles. In this model, the employer provides a set amount of cash upfront to cover all expenses. This offers flexibility but shifts the entire logistical and financial risk to the individual.

Industry reports indicate that lump-sum payments are increasingly popular among HR departments. However, for the employee, these payments are often treated as supplemental wages. This means they are subject to immediate tax withholding, reducing the actual cash available for moving.

Direct billing is often preferred by those looking to minimize out-of-pocket stress. Here, the company pays service providers—such as moving companies and airlines—directly. This model reduces the immediate financial burden but limits the ability to choose specific vendors.

The Tax Drag Reality: How State Rules Eat Into Your Raise

Salary negotiations usually center on the headline figure—the gross annual pay. However, for professionals moving across state lines, that number is often a poor indicator of take-home pay. The financial reality is frequently buried in the friction between disparate state tax codes.

Many workers only discover the true cost of a “raise” after their first paycheck arrives. By then, the move is complete and the lease is signed. What looked like a significant step forward can quickly become a lateral move once the government takes its share.

The administrative burden of these moves is equally taxing. Relocating professionals must navigate the complexity of filing partial-year tax returns in two different states. This process requires a meticulous, day-by-day apportionment of income and credits.

This dual-filing requirement represents a tangible financial risk. When two states have conflicting definitions of residency, the risk of double taxation becomes a reality. For the unprepared, these hidden costs can turn a career milestone into a source of immediate stress.

The Comparative Tax Landscape: Maryland vs. California

A common scenario involves a software engineer moving from Maryland to a tech hub in California. In this case, the professional transitions from a $95,000 salary to a $120,000 salary. On the surface, this 26% increase suggests a significant improvement in lifestyle.

However, the shift in tax regimes tells a more complicated story. Maryland’s tax structure is unique due to its “piggyback” system. While the state income tax rate is moderate, local jurisdictions levy their own income taxes on top of the state rate.

In high-population areas like Montgomery County, the local rate is typically 3.2%. When combined with the top state marginal rate of 5.75%, a resident can face a combined rate of nearly 9%. This local levy is a significant factor that many out-of-state recruiters fail to account for.

Table 3: Maryland vs. California Tax Comparison ($120k Salary)

Giniloh Interactive Calculator Walkthrough: From Lease Break to Net Gain

Financial Analysis of Career-Based Relocation

The prospect of a $25,000 salary increase often serves as a primary catalyst for relocation. On paper, a jump from $95,000 to $120,000 represents a 26.3% nominal raise. However, raw salary data rarely tells the complete story of a cross-country move.

Journalistic analysis suggests that gross figures frequently mask the complex reality of net income adjustments. When moving between distinct fiscal environments, the “raise” can be eroded by localized obligations. These factors often turn a perceived windfall into a break-even scenario.

To quantify these variables, the Interactive Relocation Calculator provides a framework for assessment. The tool moves beyond simple cost-of-living comparisons to examine specific “leakage” during a transition. This includes everything from pro-rated rent to specific state tax treatments.

In the current economic climate, the “salary illusion” remains a significant hurdle. This phenomenon occurs when an individual focuses on a higher gross number while ignoring increased costs. The following analysis examines the financial friction points of moving from the Mid-Atlantic to the West Coast.

Establishing the Baseline: The Maryland Fiscal Environment

The initial phase of any relocation assessment requires a precise accounting of current standing. In this scenario, the baseline is established using a single filing status in Maryland. This state serves as a complex starting point due to its multi-layered approach to taxation.

Unlike states with a flat tax, Maryland employs a multi-tiered fiscal structure. A critical component is the local “piggyback” tax, which is collected by the state but distributed to counties. For an individual earning $95,000, this local assessment represents a significant deduction.

The Interactive Relocation Calculator utilizes these specific parameters to determine the current “take-home” baseline. By entering a $95,000 salary, the tool accounts for federal tax, Social Security, and specific Maryland brackets. This creates a realistic picture of what the professional actually sees in their bank account.

In this example, you can enter the baseline as follows:

-

Filing Status & Origin Inputs: Select

Single. Set Origin State toMaryland. Set Origin Local Rate to3.2%. Enter Origin Base Salary as95000. -

Destination Inputs: Set Destination State to

California. Input Destination Base Salary as120000. Note that the state exceptions indicator lights up green because California excludes qualified moving costs from state taxable income.

The Relocation & Lease Break Friction

This breakdown explains the hidden financial costs (the “friction”) of breaking a current lease and moving across the country for a new job.

Lease Break Setup: Navigate to the Lease Break tab. Enter rent details: Monthly Rent 2200, Days Occupied 12. Enter Penalties 3500, Lost Deposit 1500, and Employer Allowance 2000.

* Qualified Transit Expenses: $1,800 packing/loading + $1,200 truck rental + $800 flights (all employer-reimbursed).

* Tax Status: Physical transit reimbursements ($3,800) are fully taxable federally under OBBBA rules, creating a state-level tax liability difference (tax drag) since California excludes qualified expenses.

Mastering State-Specific Tax Nuances: AB 692 and OBBBA Explained

Here’s a hard truth about job offers that include relocation: the number on your offer letter isn’t the number you’ll take home. Most people don’t realize this until they see their first paycheck. Job boards and generic career advice sites completely ignore this reality.

In my experience, the technicalities of state-specific laws like California’s AB 692 can catch even seasoned professionals off guard. These regulations dictate how income is sourced and taxed during the transition year. Failing to account for these nuances can lead to unexpected liabilities during tax season.

Furthermore, historical frameworks like the Omnibus Budget Reconciliation Act (OBBBA) have shaped how we view fiscal responsibility in relocation. While the names of the laws change, the principle remains the same. The government views your move as a taxable event, not just a career step.

Calculating Your Break-Even: The Payback Period Formula

Crunching the Real Numbers: The $6,130 Leap of Faith

Alright, let’s stop talking in hypotheticals and get our hands dirty with some actual math. For a career relocation from Maryland to California, the upfront sting is very real. Between lease breaks, moving vans, and security deposits, the initial costs can be staggering.

I often tell my clients to calculate their “Payback Period.” This is the number of months it takes for your new, higher net income to cover the total cost of the move. If your move costs $15,000 and your monthly net increase is only $500, it will take you 30 months just to break even.

In our software engineer scenario, the upfront costs totaled approximately $6,065. When you factor in the higher California taxes and cost of living, the “raise” feels much smaller. It is vital to know if you are moving for a better life or just a bigger tax bill.

Turning Data into Action: Negotiating Smarter and Planning Ahead

When the Offer Isn’t a Slam Dunk

So you’ve run the numbers. The calculator spits out a break-even of 5.0 months for that leap from Maryland to California. Seems good, right? But gazing at a raw number is like looking at a map without knowing where the potholes are.

I recommend using this data as leverage during your final negotiations. If the “tax drag” is going to cost you $5,000, ask for a signing bonus to offset it. Most companies have “relocation buckets” that are separate from salary budgets, making these requests easier to grant.

Don’t just accept the standard package. If you know your lease break is going to be expensive, ask for that specific cost to be covered. Being armed with precise data makes you a more formidable negotiator and ensures your career relocation is a true financial gain.

Conclusion: Beyond the Paycheck

So you’ve run the numbers on that shiny new job offer. Now what? Here’s the truth about career relocation: it’s never just about the salary bump. The hidden costs—tax drag, lease penalties, and state-specific rules—can quietly eat into your raise.

In my years of tracking these transitions, I’ve seen that the most successful moves are those planned with a cold, analytical eye. Don’t let the excitement of a new city blind you to the reality of your bank account. Take the time to calculate your real net gain before you sign on the dotted line.

Ultimately, a move should propel your career and your finances forward simultaneously. By understanding the regulatory landscape and negotiating for gross-ups, you can ensure your next big move is a win. Your career is an investment; make sure the relocation pays off.

FAQ

Are employer-reimbursed moving expenses considered taxable income?

Yes, under the Tax Cuts and Jobs Act of 2017, most employer-provided moving reimbursements are treated as taxable wages. This means the value of your relocation package is reported on your W-2 and is subject to federal, state, and FICA taxes.

What is a tax gross-up provision in a relocation agreement?

A tax gross-up is a provision where the employer provides additional funds to cover the tax liability generated by relocation benefits. This ensures the employee receives the full intended value of the assistance without a reduction in take-home pay due to increased withholding.

How is the relocation payback period calculated?

The payback period is calculated by dividing the total upfront costs of the move, such as lease penalties and moving services, by the monthly increase in your net take-home pay. This figure represents the number of months required for the new salary to fully offset the initial expenses of the transition.

What are the primary differences between a lump-sum payment and direct billing?

A lump-sum payment provides a fixed cash amount for the employee to manage, offering high flexibility but shifting all logistical risk and tax withholding to the individual. Direct billing involves the employer paying vendors directly, which reduces out-of-pocket stress but limits the employee’s choice of service providers.

How does moving between states affect tax filing requirements?

Relocating across state lines typically requires filing partial-year tax returns in both the origin and destination states. This process involves a precise, day-by-day allocation of income, deductions, and credits to ensure compliance with two distinct sets of state tax mandates.

Why might a significant salary increase result in a “lateral move” financially?

A nominal salary increase can be eroded by “tax drag” and regional cost-of-living adjustments, particularly when moving to a state with higher marginal tax rates. If the increase in net income is minimal compared to the higher costs of housing and local taxes, the professional’s actual purchasing power may remain unchanged.

References

[1] The qualifications to get a job as a relocation consultant include knowledge of the area in which yo.

[2] Your other job duties include consulting with the relocating employees to understand their needs, ma.

[3] Your other job duties include consulting with the relocating employees to understand their needs, ma.

[4] Browse 1000+ RELOCATION CONSULTANT jobs ($24-$92/hr) from companies with openings that are hiring no.

[5] The possibility of a lower cost of living may be the best factor to use when considering location an.