The Strategy Brief

- Transition from a static ‘bucket’ savings model to a flow-centric approach that prioritizes money velocity and the continuous movement of capital toward high-impact goals.

- Our Giniloh Frictionless Money Flow simulator utilizes a visual, node-based interactive canvas to map out the relationships between income, debt, and savings, making cascading financial effects easier to understand and manage.

- We Implemented AI-driven orchestration to translate natural language instructions into automated routing rules, ensuring your money moves according to specific logic without manual intervention.

- You can stress-test your financial plans against diverse economic regimes, such as stagflation or market contractions, to identify potential shortfalls and refine your strategy in a risk-free environment.

- In this educational tool, you can adopt boundary-based management by setting predefined safety floors and ceiling limits that automatically trigger transfers, reducing cognitive load while maintaining optimal liquidity.

Introduction: What Are ‘Money Flows’ and Why a Frictionless Simulator?

I’ve spent years looking at my bank balance as a static number—a simple score of success or failure at the end of the month. However, I recently realized that traditional financial management, with its focus on net worth or month-end snapshots, is fundamentally flawed. In my experience, money is rarely a stationary resource; its true utility is defined by its trajectory and the speed at which it moves through a personal system.

This movement, often referred to as “money velocity” in a personal context, serves as the primary engine of long-term stability. Rather than focusing on a stagnant pool of assets, I’ve found that the “flow” of capital determines how effectively we can respond to emerging opportunities and sudden obligations. When capital remains idle in low-interest environments, it loses the potential for compounding growth and the ability to mitigate high-interest debt efficiently.

Financial planners are now advocating for a fundamental shift in perspective, moving away from accumulation as the sole metric of success. They suggest that a healthy financial life should resemble a well-regulated utility grid. In this model, the focus remains on the seamless distribution of resources from the point of entry—typically a paycheck—to the point of maximum economic impact, such as a retirement fund or debt repayment.

The Shift from Buckets to Flows

This systemic approach requires a departure from the “bucket” method of saving, where money is simply piled into accounts without a clear exit strategy. Instead, the flow-centric model prioritizes the movement of every dollar. By ensuring that capital is always in motion toward a specific goal, individuals can maximize the efficiency of their earnings and reduce the time assets spend in non-productive states.

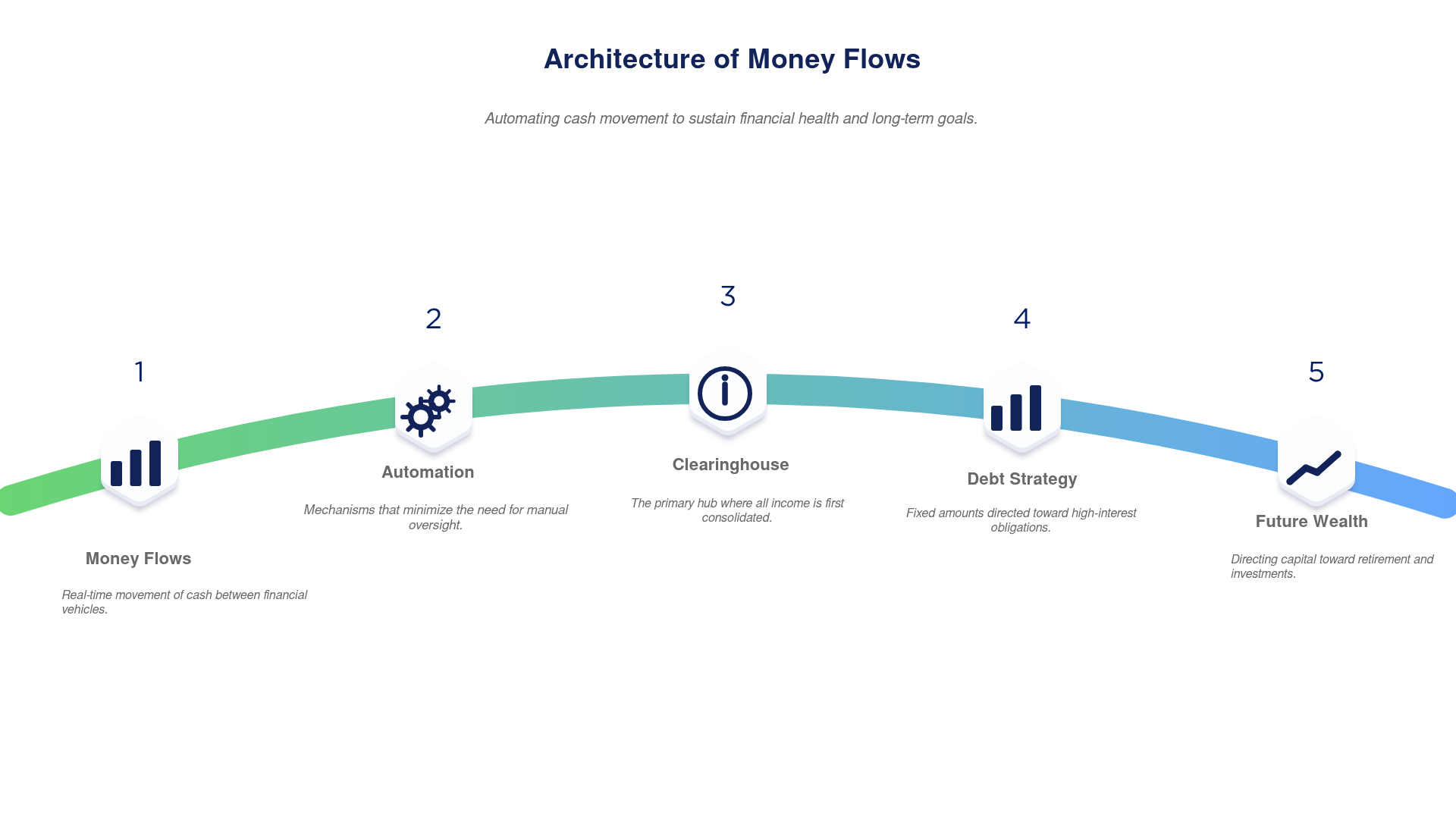

The Architecture of Money Flows

Money flows represent the real-time movement of cash between various financial vehicles, including checking accounts, high-yield savings, debt obligations, and investment portfolios. This system acts as a continuous stream of capital, ideally routed through automated mechanisms that minimize the need for manual oversight.

When functioning correctly, the system ensures that every dollar has a pre-assigned destination before it even arrives in a bank account. Industry experts often compare this process to the circulatory system of a biological organism. In this analogy, cash serves as the lifeblood, moving through different “vessels” to sustain various goals or reduce liabilities.

The Central Clearinghouse

The core of this architecture is the central clearinghouse, which is typically a primary checking account where income is first consolidated. From this hub, the “flow” is directed outward to various spokes. In a high-functioning system, these movements are governed by predefined rules rather than sporadic, emotional decisions made at the end of a long work week.

A sophisticated flow might direct a specific percentage of income toward retirement accounts, a fixed amount toward high-interest debt, and a residual portion toward liquid savings. The efficiency of this distribution determines the overall health of the system. It ensures that capital is available exactly when and where it is needed most, without the friction of manual intervention.

The Frictionless Money Flow Concept – Unified Loh-Friction Philosophy

The concept of frictionless capital movement represents a fundamental shift in the landscape of personal financial management. It marks a decisive transition from manual, reactive intervention toward a sophisticated model of automated synchronization. This evolution reflects broader trends in the modern digital economy, where efficiency and speed are increasingly prioritized.

The Unified Loh-Friction Philosophy operates on the core premise that financial assets should transition between various accounts with the same seamless efficiency as electricity moving through a smart grid. Within this framework, money is no longer viewed as a static pool of resources. Instead, it is treated as a dynamic current that must be directed with precision.

Eliminating Systemic Inefficiencies

The ultimate goal of this approach is to eliminate the systemic inefficiencies that have historically drained household wealth. Common obstacles, such as late fees, idle cash, and missed investment windows, are categorized as “friction.” This philosophy seeks to bypass these hurdles by establishing automated Money Flows that prioritize the user’s needs.

These flows are specifically tailored to individual liquidity requirements rather than the rigid, often arbitrary cycles imposed by institutional banking. This philosophy serves as the foundational logic for the Giniloh Frictionless Money Flow Simulator. The simulator is a digital environment designed to model the movement of capital through complex account structures.

The Origin of the Philosophy

The Unified Loh-Friction Philosophy did not emerge from the traditional corridors of retail banking or established fintech conglomerates. Instead, it was developed through the careful observation of systemic friction within conventional financial tools. Research into consumer banking habits indicates that standard structures often impose unnecessary delays and rigid rules .

These institutional constraints frequently result in measurable financial loss for the average consumer. Delays in fund availability, often referred to as “float,” allow banks to benefit from capital while the account holder remains unable to deploy it. The Loh-Friction approach serves as a corrective framework to address this historical power imbalance.

Reactive vs. Boundary-Based Management

In traditional models, capital management is frequently characterized by “burst” activity. These are often reactive transfers prompted by impending bills, manual savings contributions, or panic-driven movements during periods of market volatility. The Loh-Friction Philosophy replaces this reactive behavior with a boundary-based system.

By establishing predefined rules and thresholds, the system manages the flow of capital autonomously. This ensures that liquidity is maintained where it is needed most while surplus funds are directed toward growth-oriented vehicles without delay. The primary objective is to reduce the cognitive load on the individual, allowing them to focus on high-level strategy.

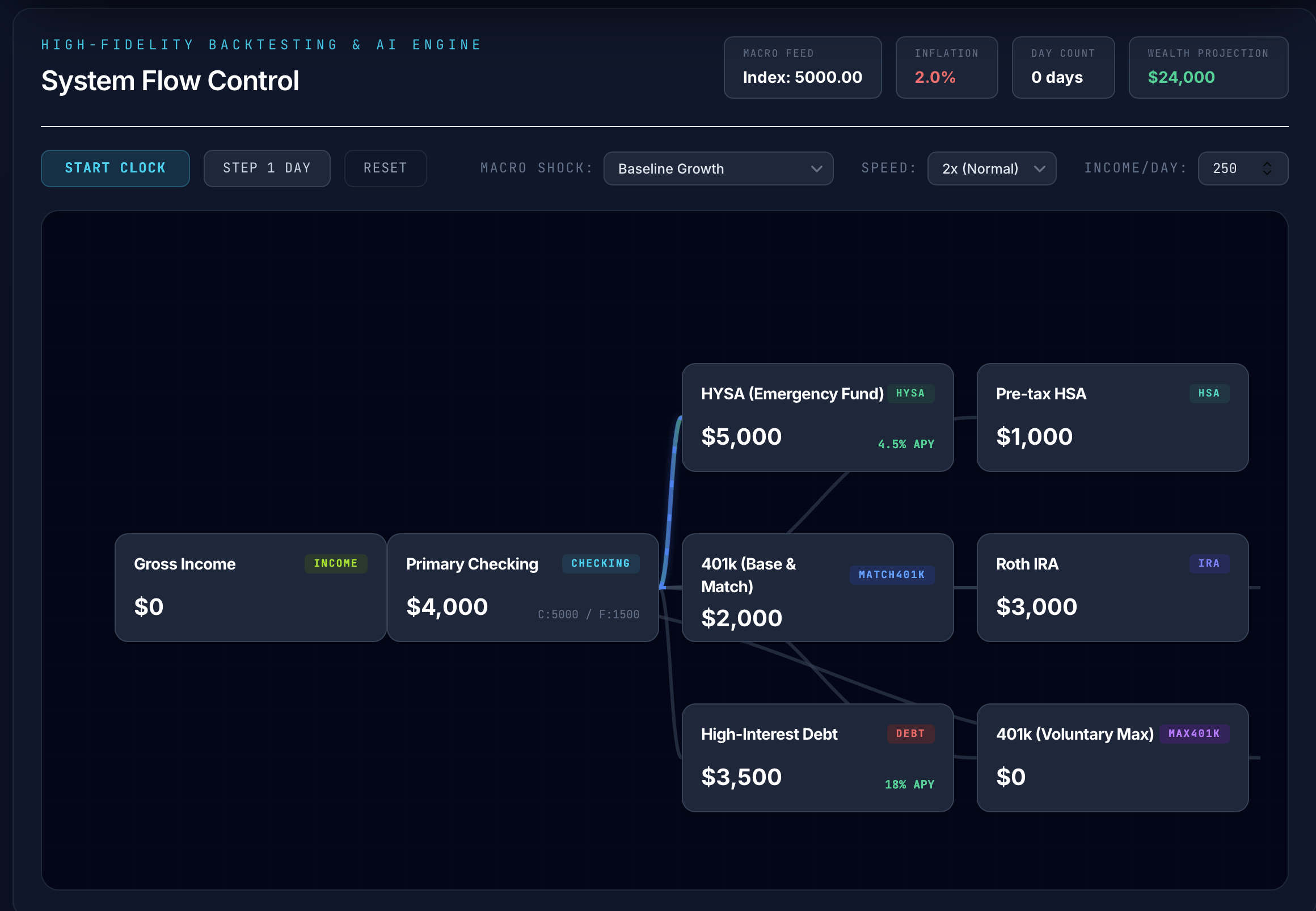

Configuring Accounts on the Interactive Canvas – Drag, Drop, and Simulate Money Flows

By utilizing a node-based architecture, the Giniloh Frictionless Money Flow Simulator allows users to visualize liquidity transitions and debt cycles. The spatial representation of a financial portfolio helps clarify how money moves between accounts over time. Configuring individual account nodes is the first step in establishing a high-fidelity simulation.

The Architecture of the Interactive Canvas

The Interactive Canvas operates on the principle of directed acyclic graphs (DAGs). In this network topology, each “node” represents a discrete financial entity. This might be a checking account, a high-yield savings account, a brokerage portfolio, or a specific debt obligation.

This visual approach addresses a common challenge in financial planning: conceptualizing cascading effects. Traditional spreadsheets require users to trace complex cell references and hidden formulas. The canvas replaces these abstractions with a literal map of money flows, making the relationship between accounts immediately apparent.

Node-Based Interaction and Parameter Management

The primary interaction model involves selecting and modifying these nodes. When a user clicks a specific account node, the system triggers a contextual interface known as a parameters drawer. This drawer typically emerges from the side of the workspace, allowing the user to keep the broader map in view.

This non-modal design choice ensures that the user maintains visual contact with the entire financial ecosystem while adjusting granular details. By reducing cognitive load, the interface allows for immediate visual feedback as variables change across the network. The architecture also supports complex “many-to-one” or “one-to-many” relationships.

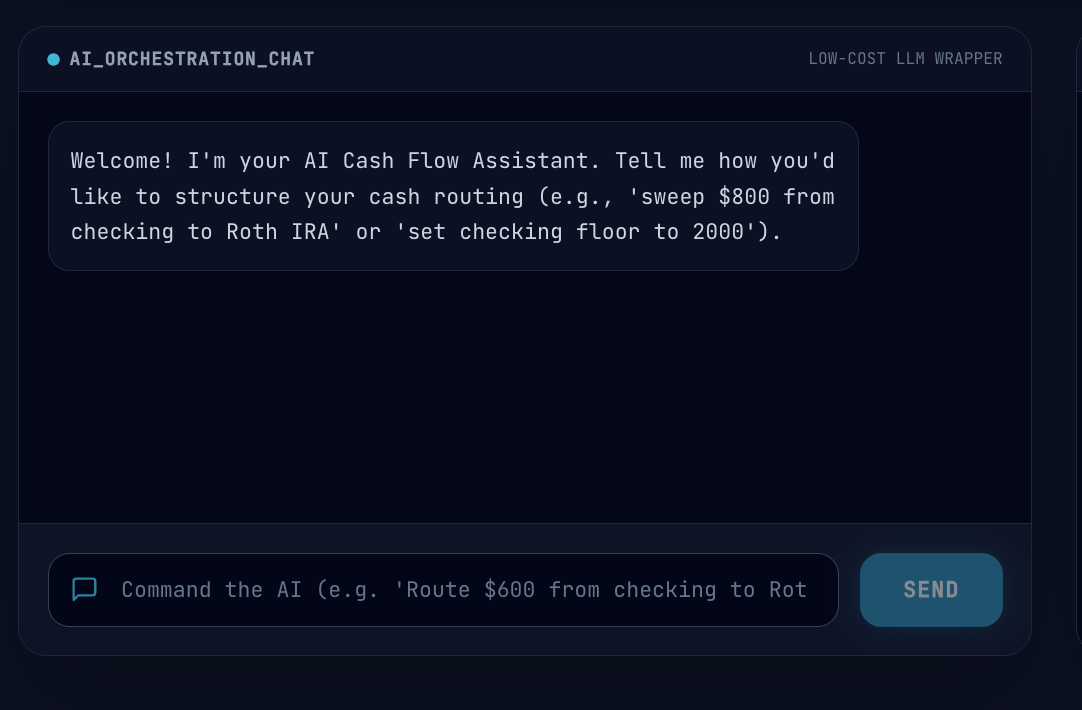

Building AI-Driven Cash Pipelines with Orchestration Chat or CLI

Orchestration Chat: Natural Language for Money Flows

The AI Orchestration Chat represents a shift toward natural language processing as a primary interface for liquidity management.

By utilizing a large language model trained on specific financial ontologies, the system allows you to execute movements of capital through standard English prose. A user might issue a directive to “Send $500 to my high-yield savings account every Friday unless my checking dips below $1,000.” The system parses this intent and translates it into executable routing rules.

The system does not merely implement static rules; it possesses the capacity to adjust routing logic dynamically based on qualitative conditions. If a user expresses a desire to prioritize debt reduction, the AI interprets the term “priority” within a specific financial framework. It then reconfigures the “waterfall”—the sequential order in which funds are allocated—to reflect that objective.

Technical Layers of Processing

The technical architecture of the Orchestration Chat involves several layers of processing. First, the natural language engine performs named entity recognition to identify accounts, amounts, and frequencies. This step ensures the system understands exactly which financial buckets are involved in the transaction.

Next, the intent-parsing layer determines the logical conditions, such as the “unless” clause. This functions as a conditional trigger that can halt or modify a transaction based on external variables. Finally, the orchestration layer maps these intents to the Money Flows API, ensuring requested actions comply with safety constraints.

Stress-Testing Your Money Flows Against Real Economic Scenarios

Operational Execution: Automated versus Manual Simulation

Integrating financial accounts into a simulation canvas requires a strategic choice in execution. Once a user sets parameters—such as a $5,000 checking account sweep threshold—the platform offers two distinct modes: automated daily processing and manual incremental stepping.

The automated daily clock runs the user’s entire cash flow logic in a single, consolidated cycle. This mode can simulate months of financial activity in seconds. For planners, this offers a fast way to see how specific money flows and routing rules perform over a fiscal year.

High-Velocity vs. Granular Auditing

High-velocity simulation is particularly effective at spotting potential shortfalls in debt service. By “running the clock” forward, users can see if their current savings rate will actually cover a future spike in expenses. This bird’s-eye view serves as the first line of defense against structural flaws in a financial plan.

Manual stepping offers a different perspective by slowing the simulation to a day-by-day pace. This allows for a close examination of the system’s decision-making process. Users can watch the exact moment a “safety floor” triggers or a “ceiling limit” stops a transfer, ensuring the logic is sound.

Cash Routing Under Three Economic Regimes

The simulator’s primary strength is its ability to model strategies against different economic backdrops. By testing a plan against various “regimes,” users can see how their liquidity rules handle market volatility or inflation. This acts as a strategic dress rehearsal for the real-world economy.

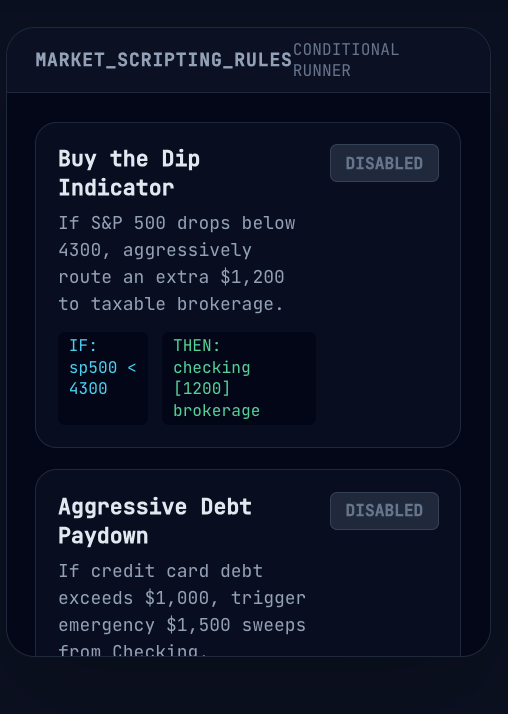

Automating with Market Scripting Rules – Conditional Money Flows

Market Scripting Rules: Simulating Real-World Constraints

This is where things get interesting—and honestly, a little addictive. The bottom-right panel of the Giniloh simulator houses the Market Scripting Rules engine. Think of it as your personal financial autopilot with a brain for macroeconomics. You’re not just watching Money Flows sit there; you are programming them to react.

These rules allow you to set “If/Then” statements based on market triggers. For example, you can script the system to accelerate debt payments if interest rates rise, or to pivot surplus cash into brokerage accounts if the market enters a specific dip. It transforms a static plan into a living, breathing strategy that adapts to the world around it.

Mastering the Control Dashboard – Adjust and Monitor Money Flows in Real Time

Look, I’ll be honest. Most financial simulators feel like doing taxes—dry, joyless, and painfully slow. But here’s the thing: the good ones let you bend time and money to your will. And that’s exactly what this dashboard does. You don’t need a finance degree or to be some Wall Street wizard to master it.

The control dashboard provides a real-time readout of every active flow. You can see the “pipes” lighting up as money moves from income to expenses to investments. If you see a bottleneck or a missed opportunity, you can adjust the sliders in real time and watch the simulation recalibrate instantly. It provides a level of clarity that makes the complex feel intuitive.

Conclusion: Why Giniloh Changes How You Manage Money Flows

Your Financial Future, Simulated Without the Risk

Here’s the thing most people don’t realize about their money—they’re flying blind until something breaks. Giniloh changes that completely. Think of it as a flight simulator for your personal economy, where you can crash and burn without losing a single dime. By mastering your Money Flows in a frictionless environment, you gain the confidence to execute those same strategies in the real world.

FAQ

How does the “money flows” model differ from traditional savings methods?

Traditional methods focus on static account balances, whereas the money flows model prioritizes the velocity and trajectory of capital. It treats money as a dynamic current, ensuring every dollar is automatically routed toward its most productive use.

Can I simulate how my finances would perform during a period of high inflation?

Yes, the simulator allows you to stress-test your strategy against various economic regimes, including stagflation and market contractions. This helps you identify potential liquidity shortfalls and adjust your routing rules before these scenarios occur in real life.

What is the purpose of the AI Orchestration Chat?

The AI Orchestration Chat allows you to manage your financial logic using natural language commands instead of complex technical settings. You can simply describe your goals, such as prioritizing debt reduction, and the AI will configure the necessary routing rules for you.

What are Market Scripting Rules and how do they work?

Market Scripting Rules are conditional “If/Then” statements that allow your money flows to react to external triggers. For example, you can script the system to automatically increase savings contributions if interest rates rise or pivot funds during market dips.

What is the benefit of using a node-based Interactive Canvas?

The Interactive Canvas provides a visual map of your entire financial ecosystem, making it easier to see the relationships between different accounts. This spatial representation helps you understand the cascading effects of your transfers and identify bottlenecks in your capital distribution.

What is the difference between automated daily processing and manual stepping in the simulator?

Automated processing runs months of financial activity in seconds to show long-term outcomes, while manual stepping allows you to audit the system day-by-day. Manual stepping is ideal for verifying that specific triggers, like safety floors or ceiling limits, are functioning as intended.

How does the Unified Loh-Friction Philosophy improve financial efficiency?

This philosophy focuses on eliminating systemic delays and idle cash, which are viewed as “friction” that drains wealth. By automating transitions between accounts based on predefined boundaries, it reduces the cognitive load on the individual and maximizes growth potential.

References

[1] In the manual, one can mint tokens, initialise pools using 5 different protocols.

[2] MoneyFlow tracks your money and how it flows in and out of your various banks and accounts.

[3] Moneyflow: Personal Finance Data Interface for Power Users (supporting backends like Monarch Money,.

[4] Money Flow has one repository available.

[5] Once uploaded, you’ll be taken to the main visualization page where you can interact with your.