The Strategy Brief

- Utilize a lease break calculator to transform vague contract penalties into precise financial projections, allowing you to compare worst-case scenarios against negotiated buyouts.

- Determine your payback period by dividing the total exit cost by your projected monthly salary increase to identify the exact date your career move becomes profitable.

- Leverage itemized data regarding your lease liabilities during job negotiations to secure specific relocation assistance or signing bonuses from your new employer.

- Prioritize a negotiated flat-fee buyout over a rent-responsible agreement to minimize financial risk and ensure a predictable exit from your current housing contract.

- The decision to terminate a residential lease agreement before its scheduled expiration is a significant financial undertaking. It requires a detailed analysis of contractual obligations, statutory protections, and market conditions. Whether driven by professional relocation or issues regarding “quiet enjoyment,” tenants face a complex array of liabilities .

The Lease Trap: One Designer’s $20,000 Dilemma

The Economic Friction of Career Mobility: A Case Study in Residential Lease Obligations

Using the Giniloh Lease Break Calculator, tenants facing a job relocation can precisely quantify worst-case, buyout, and best-case exit costs—turning an opaque penalty into a clear payback timeline that empowers them to negotiate employer funding or recover the expense.

I have spent a significant portion of my career analyzing how housing costs dictate professional freedom. Recently, I helped a designer named Sarah navigate a situation that many of us fear: a $20,000 lease liability standing between her and a dream job. In my experience, these “lease traps” are the single greatest hurdle to modern labor mobility.

In the modern labor market, geographic mobility is a primary driver of career advancement and wage growth. Professionals often find that the most significant salary jumps occur when they are willing to relocate to emerging tech hubs or established financial centers. This movement is essential for a fluid economy that matches talent with opportunity.

However, for many workers, the transition between markets is complicated by the rigid structure of residential lease agreements. These legal contracts, often signed during periods of stability, can become significant financial anchors when a sudden opportunity arises elsewhere. The friction between long-term housing contracts and short-term career opportunities is a growing concern for the American workforce.

The Austin to NYC Jump

Consider the case of Sarah, a senior product designer based in Austin, Texas. Sarah recently received an offer for a high-level position in New York City, a move that included a $20,000 annual salary increase. On paper, the promotion represents a significant financial gain, translating to approximately $1,666 in additional gross monthly income.

This increase was intended to offset the higher cost of living in Manhattan while providing a net gain in her discretionary spending power. For a mid-career professional, such a jump is often the catalyst for long-term wealth building. Yet, the logistical reality of her current housing contract presented a substantial immediate liability that threatened the entire move.

At the time of the offer, Sarah had eight months remaining on her Austin lease, with a monthly rent of $3,000. Under the strict terms of her contract, she faced a potential financial obligation of $24,000 should she vacate the property without a formal resolution. This figure represented more than her entire projected annual raise.

The Mobility Trap

The situation created an immediate liquidity crisis before she even began the packing process. This scenario illustrates a common “mobility trap” where the costs of exiting a legal contract threaten to offset the initial gains of a career move. The decision-making process for such professionals often shifts from career optimization to damage control.

Relocating workers must weigh the long-term benefits of a new role against the immediate, often jarring impact of lease termination penalties. For Sarah, the excitement of the New York offer was quickly overshadowed by the daunting math of her Austin apartment. The friction is not merely financial; it is structural and systemic.

The American rental market is largely built on the assumption of twelve-month stability. This cadence rarely aligns with the fast-moving cycles of the technology and corporate sectors. When these two timelines collide, the tenant often bears the brunt of the misalignment, facing significant debt for a home they no longer occupy.

The Financial and Contractual Implications of Early Termination

Breaking a residential lease is a complex financial maneuver that extends far beyond the physical act of moving. For many tenants, the prospect of early termination is viewed through a lens of uncertainty and fear. This often leads to paralysis or suboptimal financial decisions that can haunt a professional for years.

The primary source of this anxiety is the “early termination clause,” a standard feature in most American residential leases. This clause dictates the price of an early exit and is often written in favor of the property owner. Standard penalties for breaking a lease typically range from one to two months’ rent, but variations are common.

Understanding Acceleration of Rent

Some agreements stipulate that the tenant remains liable for the full remaining balance of the lease term until the unit is re-rented. This “acceleration of rent” can create a debt obligation that exceeds the tenant’s liquid savings. For many, this forces a difficult choice between a career-defining move and immediate financial solvency.

Transparency remains a persistent issue in the landlord-tenant relationship across the United States. Property owners and management companies are not legally required in all jurisdictions to proactively inform tenants of more economical exit strategies. This information asymmetry often results in tenants paying higher penalties than necessary.

These strategies might include flat buyout fees, subletting permissions, or lease assignments. Without this knowledge, tenants are at a distinct disadvantage during negotiations. The financial impact also includes the loss of the security deposit, which is frequently forfeited in the event of a contractual breach.

Decoding the Fine Print: Understanding Early Termination Clauses and Penalty Types

The Legal and Financial Framework of Early Termination Clauses

In the world of residential real estate, the lease agreement is the bedrock of the landlord-tenant relationship. It is a legally binding contract designed to provide a sense of predictability for both housing providers and residents. At its core, the agreement centers on the term length—typically 12 months—which guarantees a steady income stream.

However, life rarely follows a perfectly linear path. Personal and professional circumstances often shift unexpectedly. Career opportunities in distant cities, changes in family structure, or sudden financial reversals frequently force residents to consider moving before their contractual end date.

The early termination clause (ETC) is a critical component of the modern lease. This specific provision outlines the terms, conditions, and financial penalties associated with a tenant vacating the premises prior to the expiration of the lease. For many tenants, these clauses are often overlooked during the initial signing process.

Mitigating Landlord Risk

Without a clearly defined ETC, a tenant may remain legally liable for every dollar of the remaining rent due under the lease. This situation often leads to significant financial distress and can spark prolonged legal disputes. These clauses are specifically designed to mitigate the landlord’s risk, covering the costs of turnover and marketing.

The complexity of these clauses varies significantly based on state laws and the specific preferences of the property management entity. While some jurisdictions mandate a “duty to mitigate damages,” the ETC provides a predetermined “liquidated damages” amount. This allows both parties to avoid the uncertainty of a prolonged vacancy.

The Evolution of the Modern Lease Agreement

Historically, residential leases were viewed strictly as a conveyance of property interest. Under traditional common law, a tenant who walked away from a lease was often responsible for the entire remaining balance. This “no-mitigation” rule placed the entire burden of market risk on the individual renter.

Over the last several decades, the legal landscape has shifted toward a contract-based model. This evolution acknowledges that a lease is more than just a property transfer; it is a service agreement for housing. Consequently, courts and legislatures began implementing protections that require landlords to act reasonably when a tenant breaks a lease.

Today, these clauses are often standardized by state apartment associations or large-scale institutional landlords. They aim to balance the landlord’s need for the “benefit of the bargain” with the tenant’s need for a viable exit strategy. In high-growth tech hubs, these clauses have become a standard point of negotiation.

Quantifying the Financial Impact of Early Lease Termination

Quantifying Baseline Obligations and Asset Recovery

The initial phase of assessing the cost of lease termination involves the aggregation of core financial data. This includes the current monthly rent, the remaining duration of the lease term, and the total value of the security deposit. These figures form the baseline for any calculation of liability and represent the starting point for negotiation.

According to real estate industry standards, the monthly rent serves as the primary unit of measure for most penalty structures . It is imperative that tenants refer to the specific figures listed in their signed lease agreement. Relying on verbal agreements or rounded estimates can lead to significant errors in the final calculation.

Accuracy in Reporting

Even minor discrepancies in the reported monthly rate can alter the final projection by hundreds of dollars. For instance, a tenant who forgets to include a monthly pet rent or a fixed utility fee will find that their penalty calculations are consistently undervalued. Accuracy at this stage is paramount for a reliable outcome.

The number of months remaining on the lease is equally critical. This is especially true in jurisdictions where the tenant remains responsible for rent until a new occupant is secured. A common error in manual calculations is the miscounting of the remaining term, which can lead to unexpected bills months later.

Furthermore, the security deposit must be factored into the equation as a potential offset or a total loss. Under the Uniform Residential Landlord and Tenant Act (URLTA), landlords are required to return security deposits within a specified timeframe . However, the rules change significantly during an early termination.

Your Secret Weapon: A Step-by-Step Guide to Using the Giniloh Lease Break Calculator

Step 1: Set Up Baseline Lease Metrics

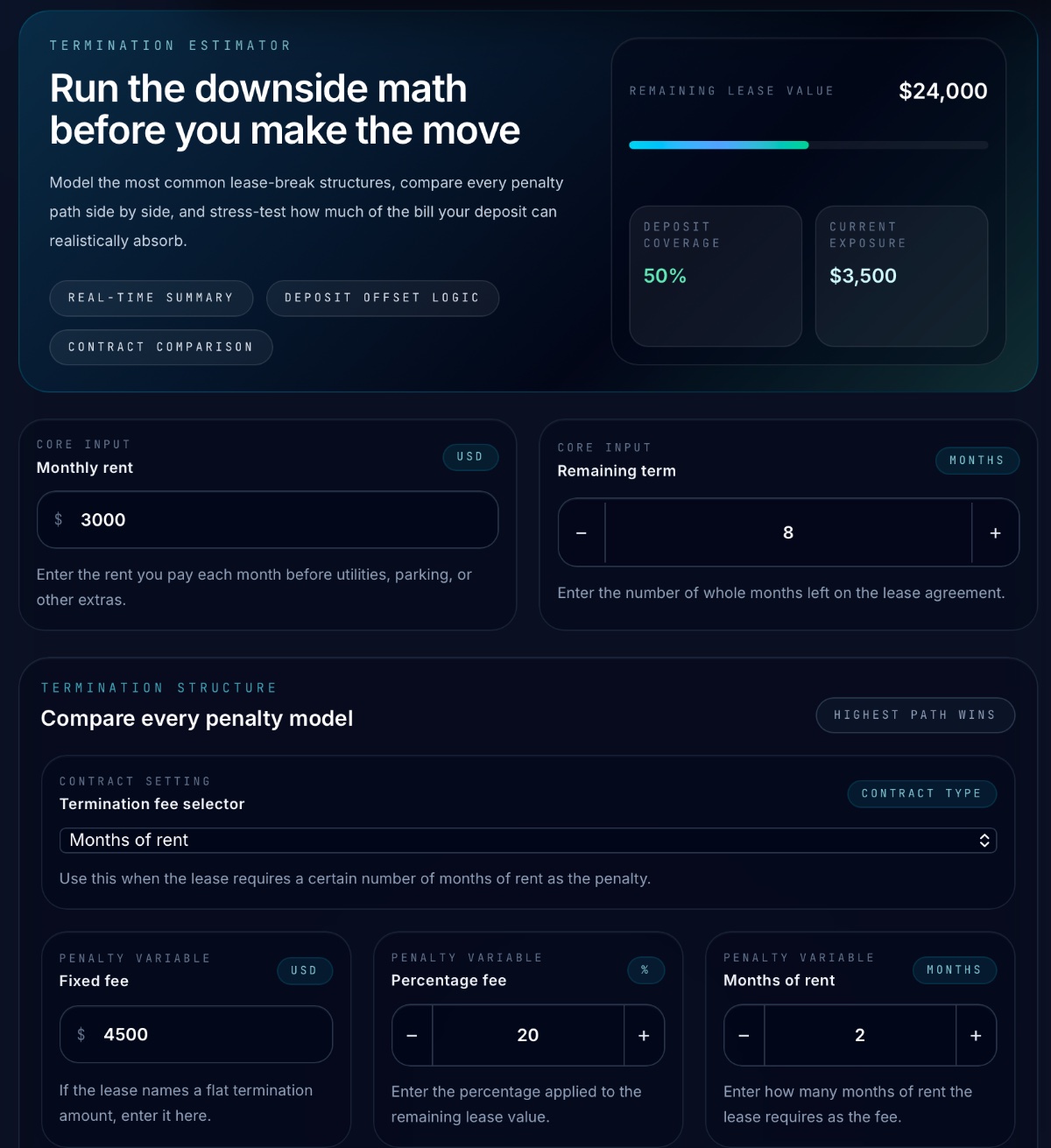

Locate the Monthly Rent field and input 3000. Set the Remaining Months stepper to 8. Notice that the dashboard immediately displays your total remaining lease liability ($24,000) at the top of the card.

Step 2: Configure the Contractual Pathways

Input the three penalty options defined in the lease agreement:

-

Set Fixed Fee Penalty to

4500 -

Set Percentage Fee Penalty to

20 -

Set Months of Rent Penalty stepper to

2

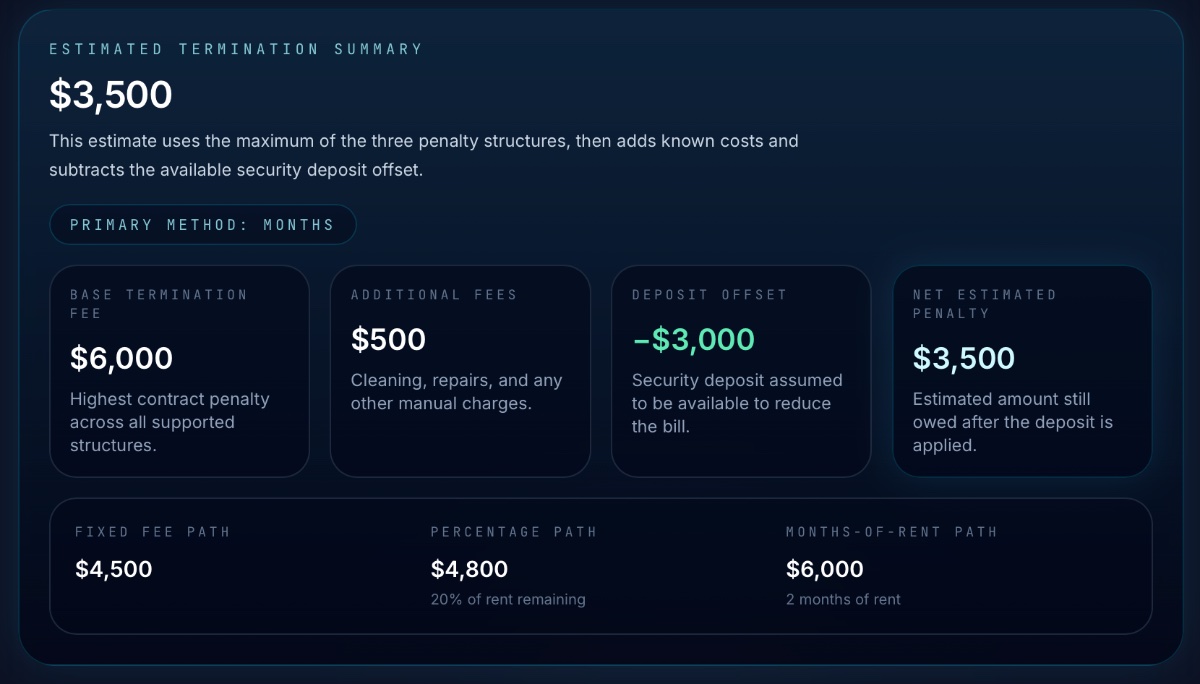

Step 3: Evaluate Scenario A (The Downside Case)

Select Months of Rent from the Penalty Calculation Method dropdown menu to model the worst-case path. Enter 500 in Additional Exit Costs and 3000 in Security Deposit. Review the summary panel to see the $3,500 Net Out-of-Pocketresult.

Step 4: Evaluate Scenario B (The Negotiated Case)

Switch the Penalty Calculation Method dropdown menu to Fixed Fee. Change the Additional Exit Costs from 500down to 150 to reflect hiring your own cleaner. Review the summary panel to see the net out-of-pocket drop to $1,650.

The Financial Reality: A Comparative Analysis of Lease Termination

The financial burden of ending a residential lease early is rarely a single, static figure. Instead, a comprehensive review of modern rental agreements reveals a tripartite cost structure that varies based on tenant action and landlord cooperation. Understanding the variance between these scenarios is essential for mitigating financial loss.

Industry analysts suggest that utilizing a standardized lease-break calculator allows individuals to project the full spectrum of potential liabilities. This data-driven approach is often the difference between a manageable transition and a significant financial setback. By quantifying potential losses early, tenants can enter negotiations with confidence.

The Strategic Advantage of a Negotiated Buyout

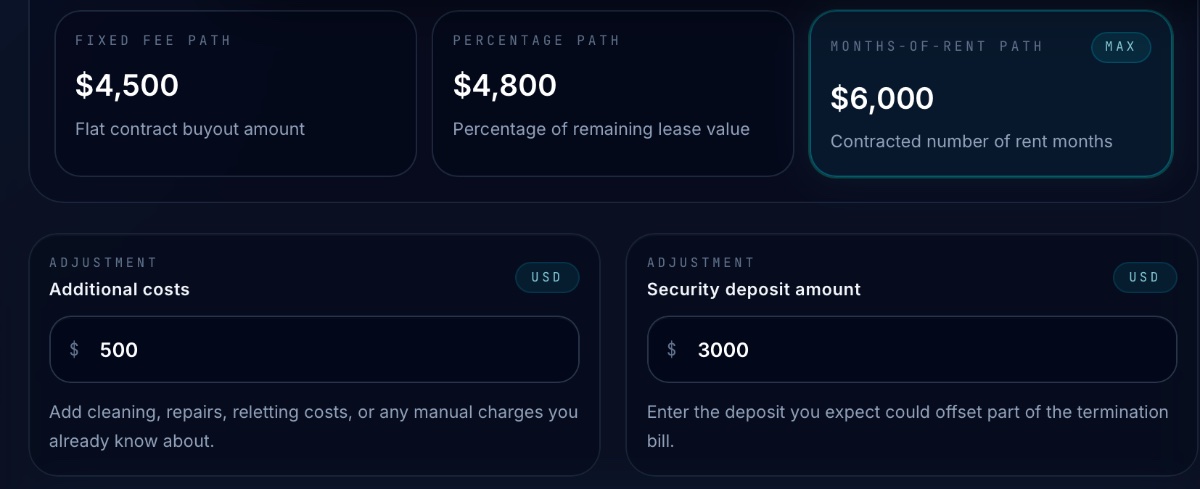

The “worst-case” scenario in lease termination often involves more than a simple penalty. It frequently includes the total forfeiture of the security deposit to cover perceived damages and administrative overhead. In Sarah’s instance, the standard penalty reached a total of $6,000.

When coupled with a $500 cleaning fee and the loss of a $3,000 security deposit, the financial burden becomes substantial. However, the data suggests that a negotiated buyout offers a more efficient exit strategy for both parties. By securing a flat $4,500 fee, Sarah reduced her net expenditure to $1,500.

This represents a 57% reduction in costs compared to the worst-case projection. Such a significant difference highlights the utility of concrete data in tenant-landlord negotiations. When tenants present a clear financial path, landlords are often more willing to accept a guaranteed payment.

The Payback Principle: How Fast You Recoup Your Exit Costs

The Mechanics of the Payback Period

In the realm of professional relocation, the “payback period” is a financial metric that functions as a strategic compass. For many employees weighing the costs of a career-advancing move, this calculation shifts the focus from the immediate penalty to the long-term return on investment.

The calculation itself is a straightforward ratio. An individual takes the total net cost of exiting their current lease and divides it by the projected monthly increase in their take-home pay. The resulting figure represents the specific number of months required to reach a financial break-even point.

This date on the calendar serves as a “finish line.” Once reached, the move has effectively paid for itself, and every subsequent paycheck contributes to the individual’s net wealth. While financial planners typically use this logic for corporate investments, it is increasingly applied to personal labor mobility.

The Psychology of the Sunk Cost

Human decision-making is frequently influenced by loss aversion. Research indicates that the psychological pain of losing money is often twice as intense as the joy of gaining that same amount. This quirk can trap professionals in suboptimal living situations.

The fear of “wasting” a security deposit often outweighs the potential benefits of a new job. The payback period serves as a cognitive tool to neutralize this bias. It replaces emotional hesitation with objective, data-driven analysis of future cash flows.

When a professional sees that a $3,500 penalty can be recovered in just eight weeks of work, the perceived loss loses its power. The fee is transformed from a barrier into a manageable, short-term hurdle that facilitates long-term growth.

Turning Data Into Dollars: How to Ask Your Employer for Relocation Assistance

You’ve crunched the numbers. You know exactly how much breaking your lease will cost—whether it’s the worst-case $3,500 or a best-case scenario. Now comes the tricky part: getting someone else to pay for it.

This is where the real magic happens. That calculator output isn’t just for your own peace of mind. It’s a negotiation tool. By presenting a clear, itemized breakdown of your relocation costs, you demonstrate professional diligence to your new employer.

FAQ

What is a lease break calculator and how does it help?

A lease break calculator is a digital tool that quantifies the financial impact of ending a rental agreement early by projecting worst-case, buyout, and best-case scenarios. It helps tenants move from uncertainty to strategic planning by providing a clear breakdown of potential liabilities.

How do I calculate the payback period for my relocation costs?

To find your payback period, divide the total net cost of breaking your lease by the monthly increase in your new take-home pay. This figure represents the number of months required to reach a financial break-even point on your career move.

What is the difference between a flat buyout fee and being rent-responsible?

A flat buyout fee is a predictable, one-time payment that provides a clean break from the contract. Being rent-responsible means you remain liable for monthly payments until the landlord secures a new tenant, which introduces significant financial risk depending on market demand.

Can I use lease break data to negotiate with a new employer?

Yes, presenting an itemized report of your lease break liability can serve as a powerful negotiation tool for relocation assistance. Employers are often more willing to provide a signing bonus or relocation stipend when presented with professional, data-driven evidence of the costs.

What happens to my security deposit if I terminate my lease early?

In many early termination scenarios, the security deposit is forfeited to cover turnover costs or administrative overhead. However, in a negotiated buyout, you may be able to apply the deposit toward the final fee to reduce your out-of-pocket expenses.

Why is it important to include pet rent and fixed utilities in the calculation?

Many landlords calculate penalties based on the total monthly payment rather than just the base rent. Excluding these additional fees can lead to an underestimation of your total liability and cause discrepancies during final negotiations.

What is the ‘duty to mitigate damages’ in a lease context?

This legal principle requires landlords in many jurisdictions to make a reasonable effort to re-rent the unit after a tenant vacates. This protection helps limit the tenant’s financial exposure by preventing the landlord from collecting rent on an empty unit without seeking a replacement.

References

[1] # What is the Difference Between Lease Termination and Lease Forfeiture? Leases don’t always run t.

[2] Browse a complete step-by-step guide on how to break the lease early and avoid any unpleasant conseq.

[3] Need to break your lease early? Learn your tenant rights, costs involved, and legal strategies to te.

[4] ## How to Write a Termination Letter to Break a Lease Early Writing a clear and respectful letter.

[5] Breaking a lease in Arkansas can cause a legal mess, but state law provides tenants with defined rig.