Key Takeaways

- Focus on the core decision factors that change the outcome for lease break

- Match the recommendation to your timeline, budget, and risk tolerance

- Revisit the decision when your inputs, constraints, or goals change

Introduction

By using the Giniloh Lease Break Calculator to compare financial scenarios, renters facing an early move can identify the most cost-effective exit strategy and even leverage concrete data to negotiate employer relocation support, turning a potential $3,500 loss into a recoverable

What a Lease Break Actually Costs You

There are few things are as stressful as the realization that you need to leave a home before your contract is up. Whether it’s a dream job offer in a new city or a sudden change in personal circumstances, I’ve seen how a lease break can feel like a financial trap. In my research, I’ve discovered that while a lease is a binding contract, the financial fallout is rarely as uniform as landlords would have you believe.

Terminating a residential lease before its expiration is a frequent reality in the American real estate market. Shifting economic conditions, labor market mobility, and personal emergencies often drive these decisions. While a lease is a binding contract designed to provide housing security for tenants and income stability for landlords, the need to vacate early often triggers significant financial liabilities.

Industry data indicates that professional opportunities or unforeseen life events usually precipitate lease breaks. However, the financial fallout of these departures is rarely uniform. The total cost depends on a mix of contractual language, state statutes, and the landlord’s speed in securing a replacement tenant.

Without a clear grasp of these variables, tenants often face charges that exceed several months of rent. The modern rental landscape is increasingly defined by flexibility, yet the legal structures governing that flexibility remain rigid. In high-growth hubs like Austin, Denver, or Charlotte, the velocity of the rental market can work in a tenant’s favor.

In stagnant markets, the same tenant might find themselves tethered to a vacant property for the duration of the original term. Journalistic analysis of housing trends shows that the rise of remote work and subsequent return-to-office mandates have created a surge in early terminations. Employees who moved to “Zoom towns” during the pandemic are now navigating the high costs of returning to urban centers.

This shift has turned lease termination from a rare occurrence into a standard line item in many household budgets. As the national median rent hovers near historic highs, the stakes for breaking a lease have never been higher. For many households, a lease represents their largest monthly expenditure and their most significant legal obligation.

When that obligation is severed prematurely, the ripple effects can impact credit scores, future housing applications, and overall financial stability for years to come. Understanding the specific mechanisms of these costs is the first step toward a successful transition.

The Hidden Costs Most Tenants Miss

When a tenant initiates an early departure, the financial impact typically follows one of three structures. The first is a flat-fee buyout, often labeled as a “liquidated damages” clause. In this scenario, the tenant pays a set sum—usually two months of rent—to be released from all future obligations.

This provides a predictable, if expensive, exit strategy. For a tenant paying a median monthly rent of $2,000, this immediate penalty represents a $4,000 expenditure. While the price is high, it offers “clean break” finality.

Landlords prefer this method because it covers the average time a unit sits vacant while removing the administrative burden of chasing monthly payments from a former resident. The second structure involves a penalty of one to three months’ rent combined with the forfeiture of the security deposit.

Administrative fees can quickly escalate the total cost. Landlords often charge for “re-letting costs,” which include marketing the unit and conducting background checks on new applicants. These re-letting fees are often calculated as a percentage of a month’s rent, sometimes reaching 85% to 100%.

Tenants are frequently surprised to find that their security deposit, intended to cover physical damages, is instead diverted to cover these operational expenses. This leaves the tenant responsible for any actual repairs out of pocket. The third and most volatile structure is the “rent-until-re-rented” model.

Under this arrangement, the departing tenant remains legally responsible for monthly payments until a new tenant takes possession. This places the entire “vacancy risk” on the tenant. In a slow market, a unit may sit empty for months, costing the tenant thousands in “ghost rent.”

Furthermore, many modern leases include “concession clawback” provisions. If a tenant received a “one month free” move-in incentive, breaking the lease often requires them to repay that discount in full. When combined with utility transfer fees and professional cleaning requirements, the cost of leaving can easily reach five figures.

Decoding Your Lease’s Early Termination Clause

The Legal and Financial Framework

Residential lease agreements serve as the foundational legal contracts of the modern housing market. These documents establish the specific rights and obligations of both housing providers and residents for a set duration. While these contracts are intended to remain in effect for the full term, shifting economic conditions often necessitate an early exit.

Industry experts note that breaking a lease is rarely as simple as handing over the keys and vacating the premises. It requires a comprehensive understanding of contractual language, state-specific statutory protections, and the financial mechanisms governing early departures. Tenants who fail to navigate these rules risk significant debt and long-term damage to their credit profiles.

The modern rental market has seen a notable increase in early terminations, driven largely by employment transfers and the rise of remote work. As residents move across state lines to pursue new opportunities, the intersection of local laws and federal protections becomes increasingly relevant. Navigating this transition requires a methodical approach to the “fine print.”

Analyzing the Contractual Framework

The first step in evaluating a lease termination involves a meticulous review of the signed agreement. Lease documents frequently utilize complex terminology that residents may overlook during the initial move-in process. To identify the conditions of departure, tenants should locate their original lease—often archived in digital formats or property management portals.

Specific sections often hold the key to a clean exit. Tenants should look for headings titled “Early Termination,” “Default,” “Surrender,” or “Liquidated Damages.” These provisions dictate the landlord’s predetermined requirements for a tenant’s early departure and serve as the primary roadmap for the dissolution of the contract.

Common stipulations include a requirement for a 30-day or 60-day notice period. Many contracts also include a specific financial penalty, such as a fee equivalent to two months’ rent. In some instances, these clauses may also mandate the forfeiture of the security deposit, a practice that varies in legality depending on the jurisdiction.

In California, the law does not strictly require an early termination clause to be present in a lease. However, when such a clause exists, it provides a clear framework for both parties to follow. This clarity can prevent the need for expensive litigation or aggressive debt collection efforts later in the process.

In the absence of specific termination language, a tenant remains theoretically liable for the rent due for the remainder of the lease term. This liability persists unless a specific legal exception applies or the landlord fulfills their duty to mitigate damages. Understanding this default liability is critical for anyone considering a move before their contract ends.

Use Case: The “New Job, Old Lease” Relocation Dilemma

Breaking a lease early can feel like a massive financial failure, but with the right data, it becomes a strategic negotiation tool. Here is how Sarah used the Lease Break Calculator to turn an intimidating contract into a seamless, employer-funded relocation.

👤 The Profile

-

User: Sarah, a Senior Product Designer based in Austin, Texas.

-

The Opportunity: A new role in New York City offering a $20,000 salary bump (which translates to roughly $1,665 more take-home pay per month).

-

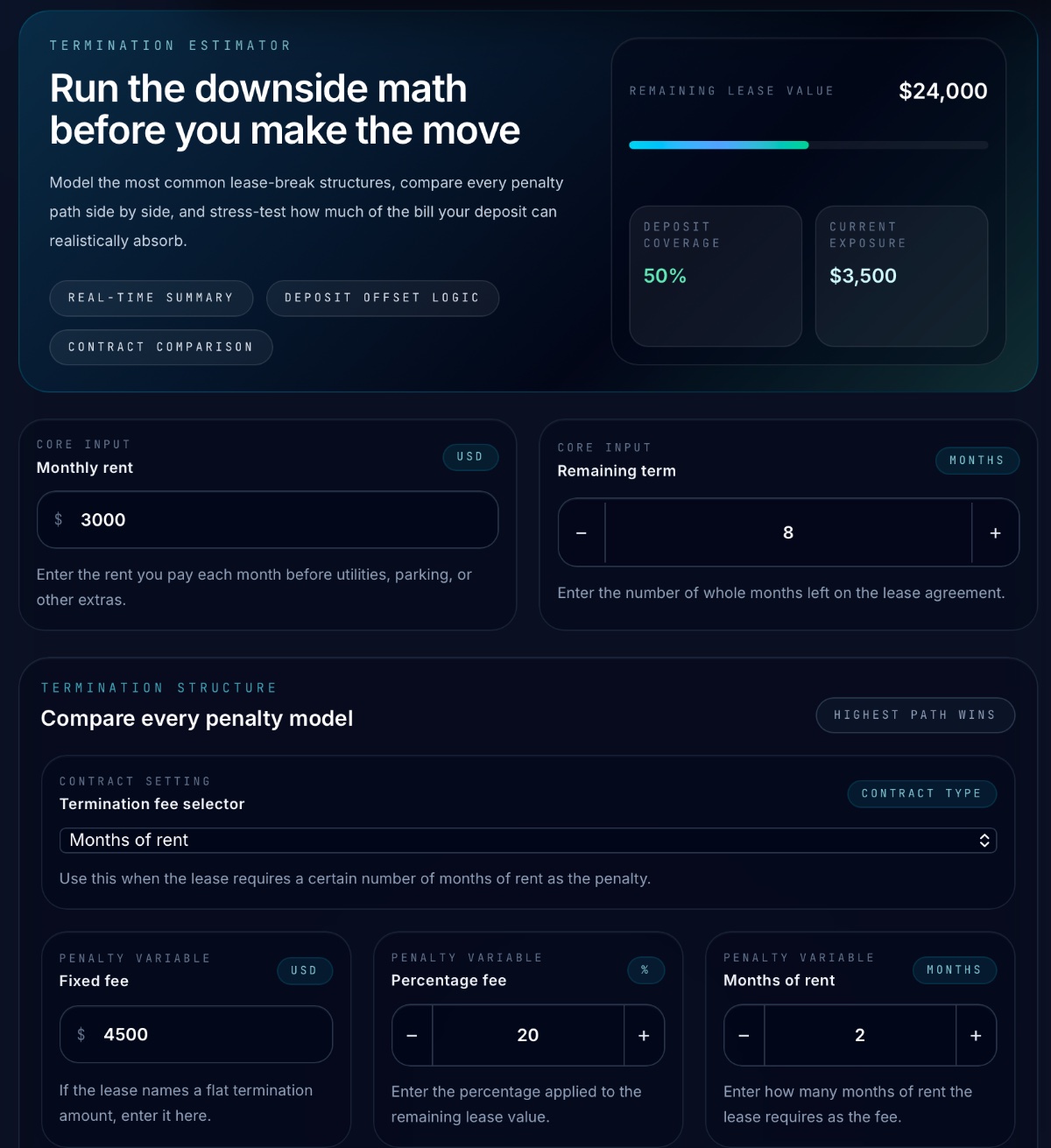

The Frictional Constraint: Sarah is only 4 months into her 12-month lease on a $3,000/month apartment. She has 8 months remaining on her contract.

-

Her Security Deposit: $3,000 (equal to one month’s rent).

The Lease-Break Contract Ambiguity

Sarah’s lease agreement contains confusing legal jargon, referencing multiple potential penalties depending on when and how she terminates. To identify her true financial exposure, she opens the Lease Break Calculator and runs a side-by-side comparison of her contract’s three penalty pathways.

The Inputs Entered:

-

Monthly Rent: $3,000

-

Remaining Months: 8

-

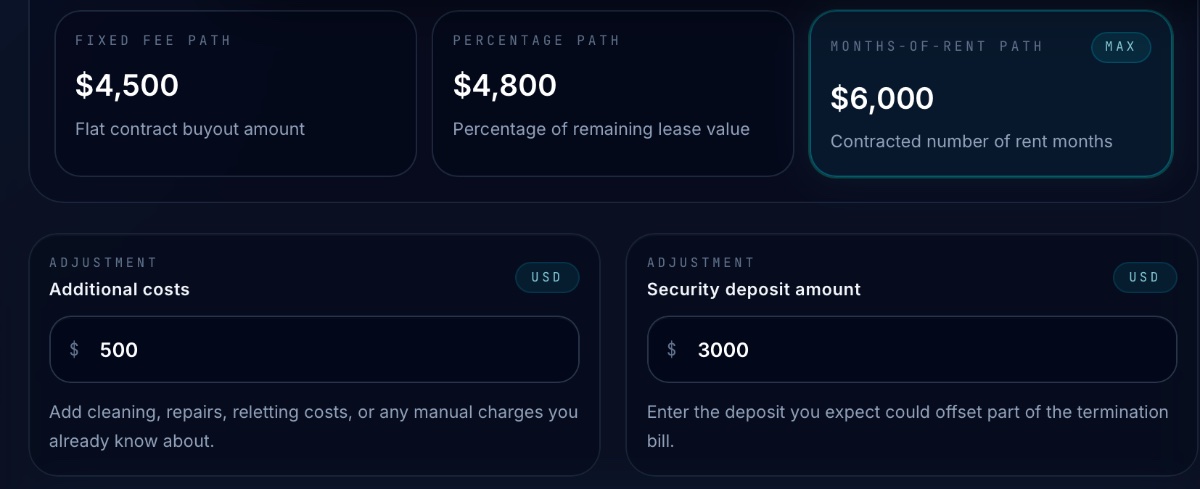

Fixed Buyout Fee: $4,500 (Stated as a flat buyout option in Addendum A)

-

Percentage Fee: 20% (Stated as 20% of the remaining lease value in Section 12)

-

Months-of-Rent Penalty: 2 months (The standard two-month notice penalty)

-

Expected Cleaning/Repair Costs: $500 (Landlord’s estimated carpet and paint patch-up fee)

-

Security Deposit: $3,000

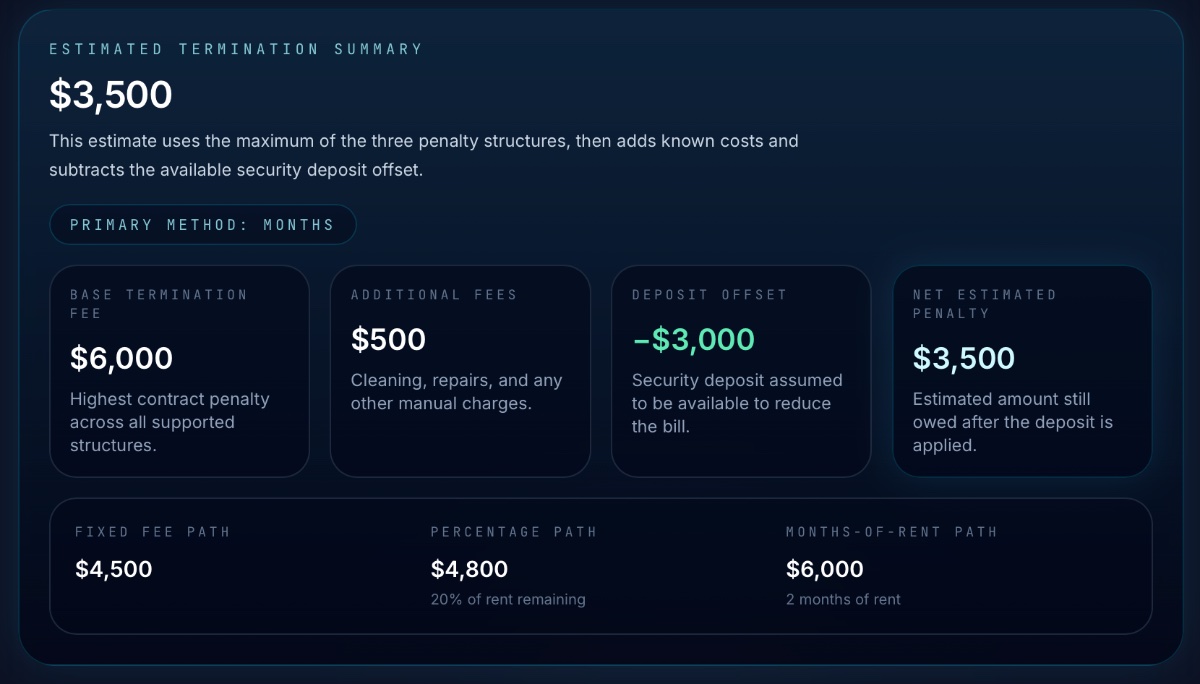

Estimated Termination Summary:

The Financial Implications of Professional Relocation

The case of Sarah, a Senior Product Designer transitioning from Austin to Manhattan, illustrates a prevalent economic friction. Economists often refer to this as the “relocation dilemma.” It is a scenario where career growth is pitted against the rigid financial obligations of a residential lease.

Upon securing her new position, Sarah received a $20,000 annual salary increase. This translates to an approximate $1,667 monthly boost in net take-home pay, according to standard tax estimates . While this represents a significant career milestone, the move was immediately complicated by her existing residential lease in Austin.

Sarah had eight months remaining on her contract at a rate of $3,000 per month. For many professionals, the process of breaking a residential lease is not merely an administrative hurdle. It is a complex financial puzzle that requires a strategic approach to mitigate potential losses.

The Liability of Standard Penalties

In a traditional lease-breaking scenario, tenants often face what financial advisors describe as a “penalty tax.” Without proactive negotiation or legal leverage, Sarah would have been subject to the standard default clauses found in many Texas residential lease agreements. These contracts are often heavily weighted in favor of the property owner.

Standard clauses typically mandate a re-letting fee or a flat penalty equivalent to two months of rent. Additionally, tenants are often held responsible for mandatory professional cleaning and administrative turnover fees. Under these terms, Sarah faced an immediate out-of-pocket expenditure of approximately $6,500.

This total comprises $6,000 in rent penalties and an estimated $500 in cleaning and administrative costs. Even after the application of her $3,000 security deposit, her net loss would have stood at $3,500. This effectively negates more than two months of her new salary increase before she even sets foot in New York.

The Payback Period: How Fast You Recover a Lease Break

The Simple Math Behind the Payback Period

In the competitive landscape of professional mobility, the financial friction of a residential lease often serves as a primary deterrent. While the immediate costs of exiting a rental agreement can appear as a formidable barrier, a rigorous analysis of the “payback period” often reveals a different economic reality. This metric measures the precise duration required for the gains from a new role to offset the capital required to exit an old lease .

The calculation functions as a straightforward linear equation. To find the break-even point, a professional divides the total exit cost by the net monthly increase in take-home pay. This shifts the conversation from a one-time “penalty” to a timed investment, allowing a candidate to see exactly when their career move transitions to a permanent financial gain.

For Sarah, her total exposure was calculated at $3,500. Her monthly income growth from a $20,000 gross salary bump resulted in an additional $1,667 in monthly gross income. By dividing the $3,500 exit cost by the $1,666 monthly increase, Sarah found her payback period: 2.1 months.

This 2.1-month figure changed her perspective entirely. It meant that within approximately nine weeks, the financial gains from her new position would fully amortize the cost of the lease termination. Beyond that threshold, every dollar of the salary increase became net positive cash flow.

Negotiating a Lower Exit Fee with Your Landlord

Quantitative Analysis and Financial Assessment

The first step in any lease exit strategy is a cold, hard look at the numbers. Tenants should begin by calculating the “total remaining liability” of their contract. This is the sum of all monthly rent payments left until the lease naturally expires, compared against the cost of a standard buyout clause.

It is also vital to distinguish between “liquidated damages” and “actual damages.” Liquidated damages are pre-set fees meant to cover the estimated cost of a vacancy. Actual damages are the real losses a landlord suffers, such as the specific days a unit sits empty and the direct costs of marketing.

FAQ

What is a liquidated damages clause in a residential lease?

A liquidated damages clause is a pre-set fee, typically equal to two months of rent, that allows a tenant to be released from their contract immediately. This provides a predictable exit cost and prevents the tenant from being liable for rent until the end of the original term.

How does the ‘rent-until-re-rented’ model affect a tenant’s liability?

In this scenario, the tenant remains responsible for monthly rent payments until a new resident signs a lease and moves in. This model places the full financial risk of a vacancy on the departing tenant, which can be particularly expensive in stagnant rental markets.

What is a concession clawback provision?

A concession clawback requires a tenant to repay any move-in incentives, such as a free month of rent, if they terminate their lease early. This can significantly increase the total cost of leaving, as it is often charged in addition to standard termination penalties.

How do you calculate the payback period for a professional relocation?

The payback period is calculated by dividing the total cost of breaking the lease by the net monthly increase in take-home pay from a new position. This helps tenants determine exactly how many months it will take for their new salary to offset the initial exit expenses.

Are re-letting fees different from standard rent penalties?

Yes, re-letting fees are specific administrative charges meant to cover the costs of marketing the unit and processing new applications. These fees are often calculated as a percentage of one month’s rent and are frequently deducted from the security deposit.

What leverage can a tenant use to negotiate a lower exit fee?

Tenants can leverage rising market rates by showing the landlord they could re-rent the unit for a higher price. Additionally, offering to help find a qualified replacement or providing significant advance notice can incentivize a landlord to reduce penalties.

References

[1] Browse a complete step-by-step guide on how to break the lease early and avoid any unpleasant conseq.

[2] Five ways to break a car lease early without overpaying.

[3] This demonstrates respect and increases the chances of finding a solution that works for both of you.

[4] Communicate with your landlord early, provide written notice 30-60 days in advance, and review any l.