The Strategy Brief

- Shift from manual budgeting to automated systems to eliminate decision fatigue and prevent emotional, fear-based financial choices during periods of market volatility.

- Implement a ‘waterfall’ structure by categorizing funds into specific buckets—such as an operating hub, safety net, and growth engine—to ensure money moves toward long-term goals automatically.

- Prioritize managing large-scale money flows and automatic ‘sweeps’ of excess cash rather than obsessing over minor daily expenses, as these strategic movements have the greatest impact on building a reservoir of wealth.

- Use financial simulation tools to model ‘what-if’ scenarios, allowing you to visualize the long-term impact of staying the course versus making impulsive changes during economic downturns.

Introduction

I remember sitting at my kitchen table on a Tuesday morning back in 2022, staring at a lukewarm cup of coffee that I’d forgotten to drink. My phone was buzzing every few minutes with news alerts, and every single one of them felt like a punch to the gut. The stock market was taking a nosedive, inflation was the only thing anyone was talking about, and my investment account looked like a sea of bright red numbers.

Personally, I used to panic during bear markets or bad economic news—and that fear cost me real dollars. My heart started racing, my palms got all sweaty, and I felt that familiar, heavy knot of dread tightening in my stomach. That’s why, at giniloh.com, we built the Money Flow Simulator to help users understand money flows in both personal and enterprise scenarios.

This tool has helped me pause and ask myself the right questions before making any fear-driven decision. I did what so many of us do when we’re scared: I made a knee-jerk move. I sold off a bunch of my holdings right when they were at their lowest point because I just wanted the “bleeding” to stop. I told myself I was being smart and “protecting” what I had left.

But you know what happened? About a week later, the market started to bounce back. While I was sitting on the sidelines, clutching my cash and feeling “safe,” I was actually missing out on the recovery. It was a cycle of regret that I just couldn’t seem to break, and I realized I was stuck in a trap of my own making.

Why Money Flow Matters More Than You Think

It took that painful loss for me to realize that I didn’t actually have a money problem; I had a money flow problem. I was reacting to the world around me instead of having a system that could handle the chaos for me. I’d spend hours worrying about things I couldn’t control, like interest rates, while totally ignoring the things I actually could control.

Once I changed how I looked at my bank account and started focusing on the way money moved through my life, everything shifted. The panic went away, and for the first time, I felt like I was actually the one in charge. Understanding your money flow isn’t about keeping fancy, complicated spreadsheets or memorizing math formulas.

It’s really just about knowing exactly where your cash is going before that “fight or flight” fear takes over the steering wheel of your life. When I talk about money flow, I’m talking about the path your money takes from the moment it hits your checking account to the moment it leaves. It’s about your savings, your investments, and your bills.

Visualizing Your Financial Plumbing

Think about your money like water in a plumbing system. If you have leaks in the pipes, it doesn’t matter how much water you pump in at the top; you’re never going to fill the tub. You’ll just end up with a soggy floor and a lot of frustration.

Money flow is about fixing those leaks and making sure the pipes are leading to the right places—like your retirement fund or your “fun money” stash. When you understand the flow, you stop worrying about the individual drops in the bucket and start focusing on the size of the reservoir you’re building for your future.

Market Analysis

I used to get that sinking feeling in my stomach every time I saw a red arrow on a stock chart. I’m talking about the kind of panic that makes your heart race and your palms sweat. During bear markets, I was a total mess. Honestly? That fear cost me a lot of real, hard-earned dollars.

I’d find myself staring at my phone at 2:00 AM, watching prices dip, and I’d eventually snap. I’d pull my money out at the absolute worst time, lock in those painful losses, and then spend the next three weeks kicking myself. It was a cycle of stress and regret that I just couldn’t seem to break on my own.

The 2:00 AM Decision Trap

I remember one specific night in a particularly nasty market dip during COVID-19 crash in 2020. Every time I refreshed my screen, a few more dollars vanished. I started doing that frantic mental math we all do—thinking about how many hours of work that lost money represented.

By 3:00 AM, I was exhausted and scared that I just hit ‘sell’ on almost everything. I thought I was being “safe,” but I was actually just letting my fear drive the car. The next morning, the market rallied, and I was left standing on the sidelines, feeling like a total failure.

Why We Built the Simulator

That’s exactly why we built the Money Flow Simulator over at giniloh.com. I’ll be the first to admit that while we built it for our users, I really built it for myself, too. I needed a way to hit the pause button and quit making those impulsive, fear-driven decisions that were wrecking my long-term goals.

This market analysis isn’t just a bunch of dry numbers; it’s about understanding the heart of how money actually moves through our lives. We’re going to look at why we do what we do and how we can set up systems that work for us, even when we’re feeling stressed. It was about turning that 2:00 AM panic into a 2:00 PM plan.

The Real Reason Most Budgets Fail

Most of us don’t actually have a “money problem” in the way we think we do. What we actually have is a decision problem. Every single time a paycheck lands in your account, you’re suddenly hit with a barrage of choices. Do you pay off a credit card, save for a rainy day, or invest?

By the time we’ve even finished weighing all those options, we’re usually mentally exhausted. Psychologists call this “decision fatigue,” and it’s a real budget-killer. When you finally sit down to “manage your money,” your brain is already fried. You don’t want to compare interest rates; you just want to stop thinking.

|

Scenario |

Manual Decision Making |

Automated Money Flow |

|---|---|---|

|

Payday Action |

Choosing where to send money |

Money moves to buckets automatically |

|

Mental Energy |

High (Leads to fatigue) |

Low (Zero effort required) |

|

Consistency |

Irregular and emotional |

100% Consistent |

|

Outcome |

Often results in “doing nothing” |

Guaranteed progress toward goals |

Investment Strategies

I want to share something with you that took me way too long to figure out. After years of making every mistake imaginable—from chasing “hot” tips to selling—I’ve realized that your actual strategy matters so much more than picking the “perfect” stock. The most important part of my plan is how I’ve set up my money flow.

I remember sitting at my kitchen table three years ago, staring at a laptop screen full of red numbers. I felt that heavy pit in my stomach, calculating how many hours of work I just “lost.” I was exhausted from trying to keep up with everything. I thought I had to be a genius, but I was just a guy with a smartphone and a lot of anxiety.

My Old Way of Making Money Decisions

I used to treat my investments like a high-stakes video game. I’d wake up, check the news before I even got out of bed, and feel this immediate pressure to do something. I felt like if I wasn’t constantly tweaking my portfolio, I was falling behind. But I wasn’t actually making smart moves; I was just reacting to noise.

I’d spend my lunch breaks scrolling through finance apps, looking for the next big thing. I’d buy a stock because a guy on a podcast sounded smart, then I’d sell it two weeks later because the price dropped 5%. It was a cycle of excitement followed by regret, and it was doing a number on my mental health.

The Cost of a Panic Sell

I remember another specific time by On Monday, August 5, 2024, where global financial markets suffered a massive “flash crash”, erasing roughly $6.4 trillion in global equity value in a single day. The market took a bit of a tumble, and the news was full of doom and gloom. I let that fear get under my skin and panic-sold a few of my solid, long-term holdings just to “protect” what I had left.

Then, a couple weeks later, those exact same stocks bounced back by 12%. Because I had jumped ship, I missed the recovery entirely. That one fear-driven choice cost me about $8000 in gains. I could have taken a nice trip with that money. Instead, it just vanished because I couldn’t keep my cool.

The Shift to Automation

That’s when things finally shifted for me. I stopped trying to be some kind of stock-picking genius and started focusing on automating my money flow into smart buckets. When your cash moves automatically toward your goals, you don’t have to rely on willpower. You don’t have to be “brave” when the market drops.

If you have to decide to save money every single month, you’re giving yourself twelve chances every year to fail. You might have a big car repair or see a cool new gadget, and suddenly that investment money disappears. But if that money moves before you even see it, the decision is already made.

What I’ve Learned from Building This Tool

Building this tool wasn’t just about coding; it was about therapy for my bank account and also a way to share my learnings and teach others. Here’s the insight that floored me: your money flow shouldn’t depend on your willpower at 2 AM when bad news hits, it should be a planned thing. The simulator is not a money plan by itself but a tool that taught me the implication of basic decisions and helped me automate the hard part—the “do I sell or hold?” debate disappears when your cash has a pre-planned path.

I used to think that being “good with money” meant having nerves of steel. But guess what? I’m not that guy. Most of us aren’t. When I realized that I could build a “digital twin” of my finances and run “what-if” scenarios, everything changed. I could see that even if the market dipped, my “floor” would keep me safe.

Focusing on the Big Flows

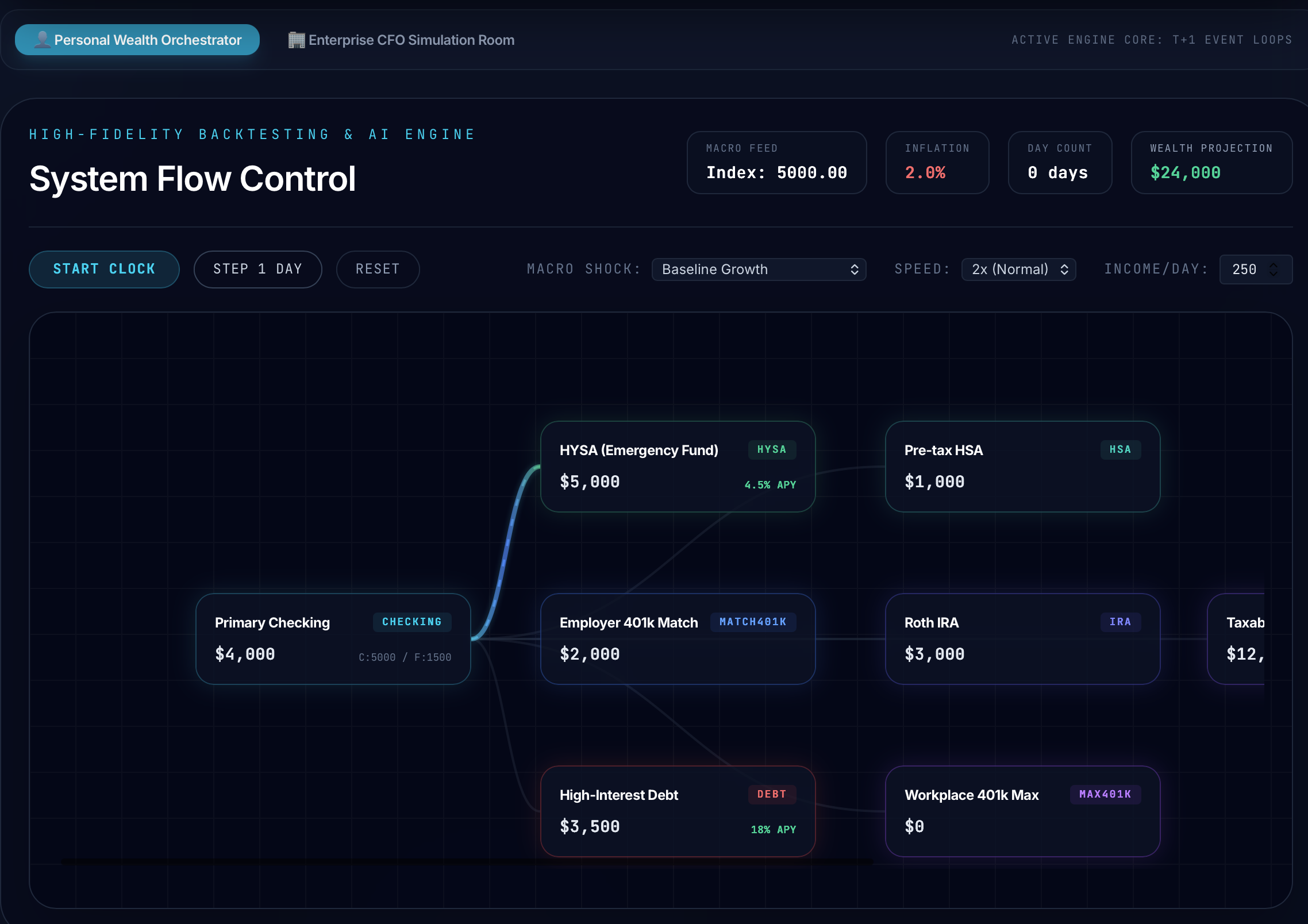

I also learned that most of us are far too hard on ourselves. I’d look at my spending and feel guilty about every coffee. But when I plugged those numbers into the simulator, I saw that those small things weren’t what was moving the needle. It was the big flows—the way I handled my “excess” cash—that really mattered.

|

Bucket Type |

Purpose |

Action Rule |

|---|---|---|

|

Operating Hub |

Daily expenses and bills |

Maintains a 1-month buffer |

|

Safety Net |

Emergency fund |

Filled before any investing occurs |

|

Growth Engine |

Long-term investments |

Receives automatic “sweeps” of excess cash |

|

Lifestyle Bucket |

Guilt-free spending |

Fixed percentage of monthly flow |

How the Waterfall Works

When we talk about money flow, I want you to picture a series of buckets. This is the “waterfall” method that the simulator helps you perfect. Most people have one big bucket where everything goes in and everything comes out. It’s messy, it’s confusing, and it’s why we never know what we can afford.

The simulator helps you set up a system where your money flows from one bucket to the next based on rules you set ahead of time. It’s like setting up a garden irrigation system instead of just throwing a bucket of water at your plants. The first bucket is your Operating Hub, and from there, the logic takes over.

Conclusion

All those sleepless nights I spent refreshing my portfolio during the last bear market—gone. Honestly, I lost money back then not because the market was crashing, but because I was panicking. I remember sitting on the edge of my bed at 3 AM, watching those red candles drop lower and lower.

The Money Flow Simulator won’t prevent a recession, but it’ll stop you from making your worst move right when you’re most tempted to throw in the towel. It acts like a mirror for your future. It shows you what happens if you stay the course and what happens if you veer off the path.

FAQ

What is a Money Flow Simulator?

A Money Flow Simulator is a tool that allows you to model and automate the movement of your finances using pre-set rules and thresholds. It helps you visualize how money moves through different accounts, such as savings and investments, to ensure your financial goals are met without manual effort.

How does automation prevent panic-selling during market dips?

Automation removes the emotional component of financial management by executing pre-planned strategies regardless of market conditions. By relying on a system rather than willpower, you avoid making impulsive, fear-driven decisions during periods of high volatility.

What is the ‘waterfall’ method of money management?

The waterfall method is a system where funds flow sequentially through prioritized ‘buckets’ based on specific rules. Money first fills your Operating Hub for daily needs, then overflows into a Safety Net, and finally moves into Growth Engines or Lifestyle accounts once thresholds are met.

How does this system address decision fatigue?

Decision fatigue occurs when the constant need to choose where to allocate money exhausts your mental energy, often leading to inaction. Automating your money flow ensures that your financial plan is executed consistently every payday without requiring active choices or willpower.

What are the four primary buckets in a money flow system?

The system typically consists of an Operating Hub for bills, a Safety Net for emergencies, a Growth Engine for long-term investments, and a Lifestyle Bucket for discretionary spending. This structure ensures that your essential needs and future security are funded before you spend on non-essentials.

Can the Money Flow Simulator be used for business finances?

Yes, the simulator is designed to handle both personal and enterprise scenarios. It allows business owners to set intelligent thresholds for operational expenses, tax reserves, and reinvestment, ensuring a healthy and predictable cash flow.

How does money flow management differ from traditional budgeting?

Traditional budgeting often focuses on tracking past expenses, while money flow management is a forward-looking system designed to direct future income. It shifts the focus from recording numbers to designing a logic-based architecture that manages your money automatically.

Do I need a high net worth to implement these automation rules?

No, the principles of money flow automation are effective regardless of your income level. The goal is to establish a functional ‘plumbing’ system for your finances so that every dollar is directed toward its most productive use as soon as it is earned.