Key Takeaways

- Transitioning from reactive tracking to proactive simulation allows you to anticipate future financial obstacles and avoid the stress of payday panic.

- Automating your money flow reduces decision fatigue by eliminating the need for constant manual transfers and repetitive mental math.

- Utilizing a risk-free sandbox environment lets you test various financial scenarios and fire drills without the danger of real-world penalties or overdraft fees.

- Incorporating regulatory guardrails into your financial planning ensures that your automated strategies remain compliant with tax laws and contribution limits.

- Visualizing your finances as a forward-looking map helps you understand exactly how today’s spending decisions will impact your future balance weeks in advance.

Introduction: Why Your Money Flow Needs a Test Drive

At giniloh.com, we built the Money Flow Simulator to help users understand money flows in both personal and enterprise scenarios. Personally, I used to panic during bear markets or bad economic news—and that fear cost me real dollars. This tool has helped me pause and ask myself the right questions before making any fear-driven decision.

I’ve been thinking a lot about money lately. Not just how much is in my bank account, but where it actually goes. You know that feeling when payday arrives and somehow, before you’ve even blinked, the balance has magically disappeared?

I’ve been there more times than I’d like to admit. It’s that weird, sinking feeling in your stomach when you look at your phone, see a double-digit balance, and realize you still have ten days left until the next check hits.

The Payday Vanishing Act

I used to call it the “payday vanishing act,” and honestly, it felt like a curse I couldn’t break. I would work forty or fifty hours a week, feel like I was being responsible, and then suddenly find myself scrounging for change to buy gas on a Tuesday morning.

It wasn’t that I was buying Ferraris or gold watches; it was just that my money seemed to have a mind of its own. It was like trying to hold water in my cupped hands—no matter how tight I squeezed my fingers, it just kept leaking out.

Here’s what I’ve realized: your money flow—the way cash moves in and out of your life—is everything. It’s the quiet engine running behind every bill payment, every latte, and every savings deposit.

Shifting from Reactive to Proactive

Most of us manage our money backward. We react to what’s already happened, checking our accounts after the fact and wondering where it all went. We treat our bank accounts like a rearview mirror, looking at yesterday to guess what we can do today.

But if you’re driving a car, you don’t just look in the rearview mirror. You need to see the road ahead. You need to know if there’s a giant pothole coming up in three weeks that’s going to pop your financial tires.

The Problem with Guessing Your Way Through Finances

I used to juggle everything manually. I’d transfer a bit to savings, hope I didn’t hit my overdraft, and cross my fingers that the credit card payment would clear before rent came out.

It was a constant game of mental math that I was usually losing. I’d be standing in the grocery store aisle, staring at a bag of fancy coffee, trying to remember if the electric bill had already been auto-paid or if that was happening tomorrow.

That kind of stress adds up. It’s not just about the money; it’s about the “brain space” it takes up. Decision fatigue is real. When you’re constantly making tiny choices about whether you can afford a sandwich, you run out of energy for the big stuff.

Studies show that simulating financial scenarios without real-world stakes rewires how you think about money. This makes so much sense to me now. When we use a tool to “test” a choice, our brains learn the patterns without the panic.

Why Your Money Flow Feels Stuck (And How to Break the Cycle)

I used to be absolutely obsessed with my Sunday night routine. I’d clear off my kitchen table and open this massive, colorful spreadsheet I’d spent hours building. I felt so smart typing in every single receipt from the week.

But that feeling of being in control never seemed to last past Monday morning. By Tuesday afternoon, I’d usually find myself standing in the checkout line, frantically refreshing my bank app to see if my gym membership fee had come out yet.

The Retrospective Panic Cycle

My spreadsheet was amazing at showing me what I’d already spent, but it didn’t do a single thing to help me in the moment. It was like looking at a map of where I’d been while I was currently lost in the woods.

That’s the big problem with how most of us are taught to handle our cash. It’s almost entirely reactive. We wait until the end of the month to see that we spent way too much on takeout, but by then, the money is already gone.

I call it the “retrospective panic” cycle. You look at the damage, feel bad about it, promise yourself you’ll do better next time, and then end up doing the exact same thing next month. It is a tiring way to live.

The Hidden Cost of Decision Fatigue

I want to tell you about something that totally changed my perspective: “decision fatigue.” It’s basically the concept that we only have a limited amount of “choice energy” every single day.

When you spend that energy worrying about small bills, you have nothing left for the big decisions. I realized that tracking my money wasn’t the same thing as managing it. I needed a system that worked as hard as I did.

The Frictionless Money Flow Simulator: A Risk-Free Sandbox

I’ll be honest with you—for years, I managed my money by staring at my bank balance and manually shuffling cash between accounts. It felt like I was constantly playing a game of financial Whac-A-Mole.

Every time I thought I had things under control, a new “surprise” bill would pop up and ruin my week. I’d forget a subscription or miscalculate a transfer, leading to constant stress.

A Flight Simulator for Your Bank Account

Then I found a way to test my money flow without any real-world risk. It’s like a flight simulator, but for your bank account. It gave me the freedom to mess up and try new things without the fear of a $35 overdraft fee.

Think about how much time we spend just moving money around. You get paid in one account, move some to savings, and maybe send a little to an investment app. Every one of those steps is a chance to make a mistake.

The Loh-Friction Philosophy: Automating Smart Decisions

How is the Loh-Friction Philosophy implemented in Giniloh Frictionless Money Flow Simulator?

The Unified Loh-Friction Philosophy is the core architectural framework of this application. It is designed to eliminate the cognitive, emotional, and structural barriers that cause individuals to fail at wealth building. Traditional budgeting is retrospective—it forces you to categorize past mistakes, inducing guilt and decision fatigue. The Loh-Friction philosophy flips this, focusing on prospective, automated wealth routing.

Here is how the philosophy is implemented practically across the app’s features and simulation engine:

1. The Dynamic Buffer: Floors and Ceilings

The simulation engine manages your everyday checking account using two simple, automated triggers:

The Overbalance Sweep (The Ceiling): You set an upper limit for your checking account—say, $3,500. The moment a paycheck drops and pushes you past that limit, the system automatically sweeps the extra money out of checking and routes it into your investments. This stops your money from sitting idle and earning 0% interest.

The Underbalance Pull (The Floor): You also set a safety floor—say, $1,500. If a big mortgage payment or a string of bills drops your balance below this number, the system instantly pulls cash from your high-yield savings account to top you back up. It completely eliminates overdraft fees and the anxiety of a low balance.

2. The Financial Waterfall: How Money Moves

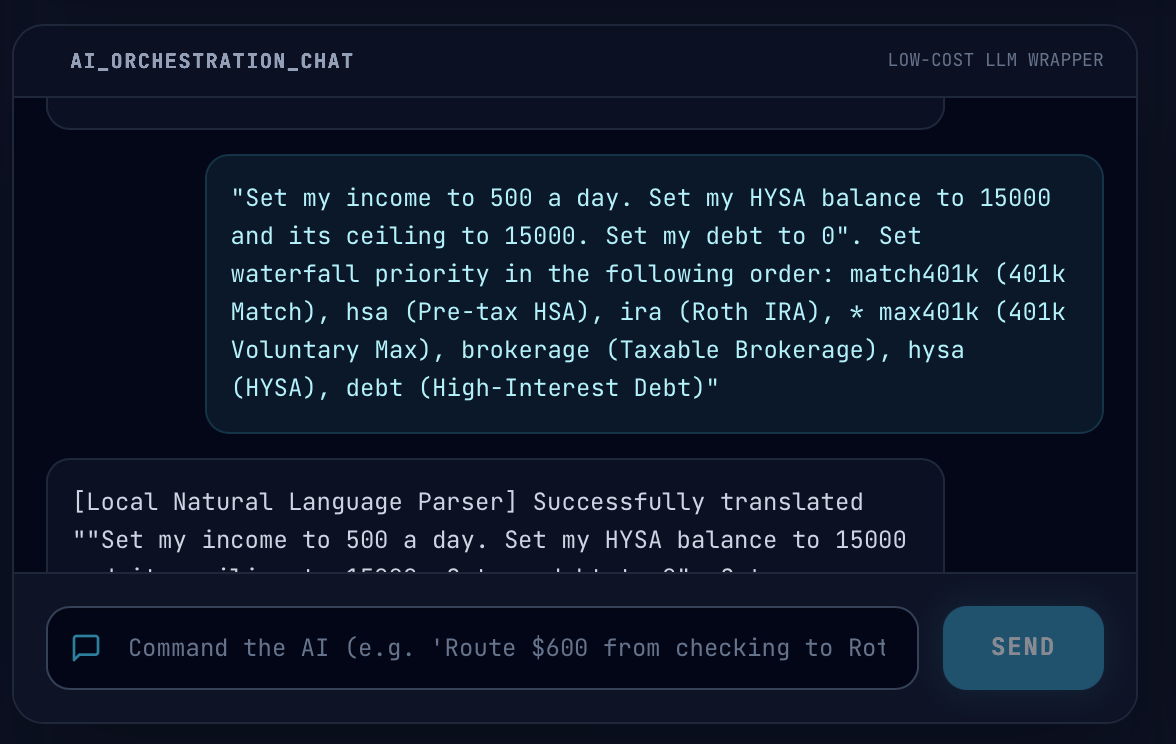

When you have extra cash, the system routes it step-by-step to make sure every dollar works as hard as possible. You can easily change this order in the UI or command line, but the default sequence follows the smartest financial playbook:

Free Money First (match401k): It instantly captures your employer’s 401(k) match.

Kill High-Interest Debt (debt): It aggressively targets and wipes out toxic credit card balances.

The Safety Net (hysa): It tops off your emergency fund until it hits your target comfort level (like $15,000).

The Tax-Free Trifecta (hsa): It routes funds into your HSA for pre-tax, tax-free growth, and tax-free spending on healthcare.

Retirement Maxing (ira / max401k): It fills up your Roth IRA and voluntary workplace contributions.

The Wealth Compounder (brokerage): Any leftover overflow pours directly into a standard taxable brokerage account.

3. Real-World Rules and Behavioral Guardrails

To help you build actual financial discipline, the app mirrors the friction, restrictions, and rules of the real world:

Locked Retirement Funds: The system locks down retirement accounts like your IRA, blocking you from easily sweeping money back out of them. It trains you to treat retirement money as strictly non-liquid.

Day Trading Boundaries: If an account has less than $25,000 in equity, the system caps equity sweeps to twice a day, keeping you compliant with real SEC Pattern Day Trader rules.

Realistic Transfer Latencies: Money doesn’t move instantly in the real world. The app enforces real bank delays—like a 6-day hold for standard ACH transfers into your brokerage, or a 15-day hold for full ACAT account transfers.

The “Panic Button” Safeguard: During a simulated market crash, the app deliberately pauses everything on Day 18 (right after a 10%+ drop). Before you can touch your portfolio, it forces you to walk through an emotional centering checklist. It’s a brilliant way to practice staying calm instead of panic-selling your assets.

4. Zero-Friction Setup: The AI Assistant

To keep you from getting bogged down in menus and settings, the app uses a smart AI console:

You can just talk to it like a person: type things like “prioritize paying off debt” or “set my checking ceiling to 3500.”

The system parses your text, converts it into backend logic behind the scenes, and instantly rewires your financial waterfall right on the visual dashboard.

I used to feel like my money was always one step ahead of me. Every payday brought the same mental gymnastics: how much to save, what to pay off first, and whether I could afford a treat.

That friction—that constant tug-of-war—was exhausting. I’ve learned it’s the single biggest thing standing between most of us and a smooth money flow. It’s the invisible weight that makes every financial move feel like a chore.

Removing the “Kinks” in the Hose

Friction is anything that slows down or blocks your money from moving where it should go automatically. It’s the hesitation when you’re deciding whether to transfer that extra fifty bucks to savings.

Think about a garden hose with a bunch of kinks in it. The water is there, but nothing is coming out the other end. That’s what friction does to your financial life. You might have the income, but the “kinks” stop the flow.

When we talk about reducing friction, we’re talking about smoothing out that path. It’s about making the right choice the easiest choice—or better yet, the only choice that happens automatically.

Test Your Smart Money Decisions: Real Scenarios

I’ve been running my own mini financial simulations long before I knew there was a fancy name for it. It all started with a broken washing machine and a maxed-out credit card.

I remember standing in my laundry room thinking: “If I’d just practiced this moment—like a fire drill—maybe I wouldn’t feel so panicked right now.” That’s the whole point of simulating your money decisions.

Creating Your Financial Fire Drill

We have fire drills at school so we know exactly where the exits are when things get smoky. Why do we usually wait for a real-life financial disaster to figure out how we’ll handle one?

I decided to stop winging it. I started treating my bank account like a game of strategy. I stopped reacting to crises and started predicting them, giving myself an “undo” button for my biggest financial regrets.

Regulatory Guardrails: How the Simulator Keeps You Compliant

The Hidden Trap Most Simulators Miss

Many tools let you dream big without checking the rules. However, real-world money flow is governed by strict limits and tax laws. If your simulation doesn’t account for these, it isn’t a plan—it’s a fantasy.

Key Regulatory Rules Built Right In

This Edge Keeps Your Strategy Real

You know what I love most about this? It keeps you from making “illegal” moves in your head. By building these guardrails into the flow, you ensure that your automated strategy is actually executable in the real world.

Real-Time Visualization: See Your Cash Flow Pipelines

I vividly remember that Sunday-night panic. I’d be sitting at my kitchen table, staring at my phone’s bank app, mentally walking through the next two weeks of bills. It was pure guesswork, honestly.

That reactive scramble—that “hope and pray” method of banking—is exactly what the Giniloh Money Flow Simulator is designed to kill for good. I want to walk you through why this changed things for me.

Mapping the Route Ahead

When we want to get somewhere, we use a map. We don’t just look at our current GPS coordinates and guess where the turns are. We look at the whole route, the traffic, and the construction.

Why weren’t we doing that with our money? The Giniloh Simulator isn’t a record of where you’ve been; it’s a map of where you’re going. It turns scary numbers into a clear, visual path.

The End of “Guessing in the Dark”

Most of us manage our money by looking backward. It’s like trying to navigate a winding mountain road at night without any headlights. You only see the pothole after you’ve already hit it.

That’s exactly how those annoying overdraft fees happen. You don’t realize you’re short on cash until the bank sends you that “insufficient funds” notification. Visualization changes that dynamic entirely.

From Simulation to Action: Taking Control

I remember the first time I stared at my bank balance and had absolutely no idea what was about to happen next. Payday was three days away, and I was just hoping nothing else hit before Friday.

By using a simulator, I moved from “hoping” to “knowing.” I could see exactly how a $200 transfer today would affect my balance in three weeks. That clarity is the ultimate antidote to financial anxiety.

Conclusion: Stop Idling, Start Moving Your Money Forward

Your Money Flow Deserves a Test Drive

I remember the first time I tried to get serious about my finances. I sat down with a spreadsheet and about fifteen different “systems” I’d read about online. It was overwhelming and ultimately ineffective.

Don’t let your financial future be a leap of faith. By simulating your money flow, you can identify the kinks in your hose, avoid regulatory traps, and finally build a system that runs on autopilot.

FAQ

What is a money flow simulator and how does it work?

A money flow simulator is a digital sandbox that allows you to model how cash moves through your accounts in real time. It helps you visualize future balances and test financial decisions without any real-world risk or impact on your actual bank accounts.

How does proactive money management differ from traditional budgeting?

Traditional budgeting often looks backward at past spending, whereas proactive management focuses on future pipelines and automated sweeps. This shift allows you to anticipate upcoming expenses and avoid financial obstacles before they occur.

Does the simulator account for legal contribution limits and tax rules?

Yes, the tool includes regulatory guardrails for accounts like Roth IRAs, 401(k)s, and HSAs. It flags potential over-contributions or penalties to ensure your simulated strategy is realistic and compliant with current laws.

How can simulating financial scenarios reduce daily stress?

By testing outcomes in advance, you remove the need for constant mental math and daily micro-decisions regarding your balance. This reduces decision fatigue and provides clarity on how current spending affects your future financial health.

What are ‘kinks’ in a money flow, and how are they fixed?

Kinks are points of friction, such as manual transfers or hesitations, that prevent money from reaching its intended destination efficiently. Identifying these allows you to smooth out the path through automation, making the right financial choice the default action.

Can I use the simulator for business or enterprise scenarios?

The Money Flow Simulator is designed to handle both personal and enterprise cash flow scenarios. It provides a scalable way to understand complex money movements and automated sweeps regardless of the account type.

References

[1] Interactive correspondent banking flow simulator + comprehensive 5-page cheat sheet covering cross-b.

[2] Contribute to LiquidityProtocol/AMM-Simulator development by creating an account on GitHub.

[3] Cash-flow simulator for your life.

[4] g0v-money-flow has 4 repositories available.

[5] Transaction Visualization: Generate interactive graphs of your financial transactions, allowing you.